Rating: High school and post-secondary

Summary: Markham interviews Heymi Bahar, the International Energy Agency’s senior analyst for renewable energy markets and policy and lead author for “Renewables 2020 Analysis and forecast to 2025.” Correction: the study was released on Nov. 10, not Nov. 17 as Markham says at the start of the conversation.

Related links:

- Renewables 2020 Analysis and forecast to 2025

- Move over Alberta gas, wind and solar now the cheapest form of energy – video interview with Dr. Blake Shaffer, University of Calgary

- EV batteries, wind and solar, and the Netherlands power grid – video interview with Baerte de Brey, with ElaadNL, the Netherlands knowledge and innovation centre in the field of Smart Charging

- Canadian energy experts prefer wind, solar – study – video interview with Dr. Tom Green, David Suzuki Foundation

- Texas power outages due to frozen natural gas infrastructure, not wind turbines – video interview with Dr. Joshua Rhodes, University of Texas at Austin

This interview has been lightly edited.

Markham Hislop: Welcome to another episode of Energi Talks, the podcast where we discuss global energy issues and trends with experts from around the world. I’m going to be discussing the International Energy Agency’s 2020 renewable energy study (released Tuesday, November 10, 2020) with lead author Heymi Bahran, who is based in Paris. He’s the IEA senior analyst for renewable energy markets and policies.

Let’s start with an overview of your study.

Heymi Bahran: The study looks at the forecast for renewables in three sectors – electricity, heat, and transport – all of them equally important. And the main result of the forecast shows us a very positive development for renewable electricity and how it deals with the [climate] crisis.

We basically found that renewables in electricity are resilient, almost immune to the crisis [COVID-19 pandemic] compared to other fuels. This is the opposite trend because while renewables in electricity generation is expecting to be reduced by 7%, overall other fuels are expected to decline in 2020.

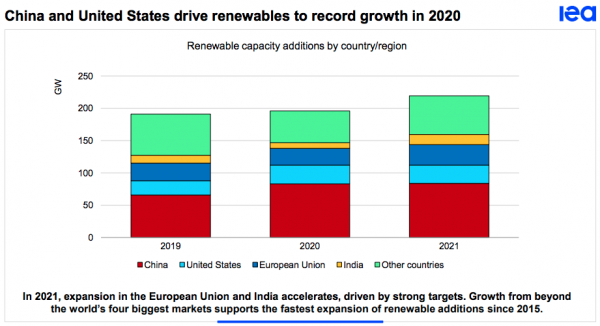

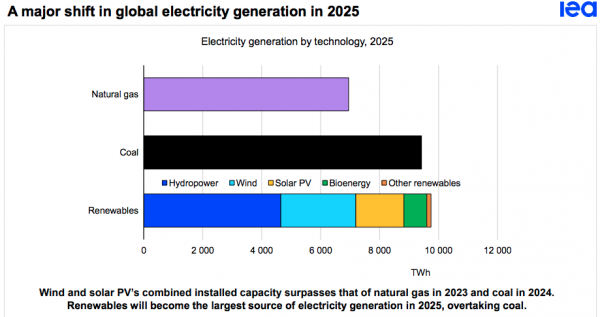

The second point is that not only that renewable generation will grow, we also look at new edict capacity to the system. So new plants, we also found out that that also is going to increase, which means that the expansion rate of renewables will continue to increase. We expect about 200 gigawatts to be installed, this year of renewable plants, including all renewables. And this is an incredible development because it accounts for about 90% of the increase in global electricity capacity, which is making up a lot of the share, which is quite important and proves the resilience.

Markham Hislop: Now a couple of weeks ago, I had American economist, Tony Seba on the podcast, and he had put out a study in which he forecast that by 2030, the combination of wind solar and battery storage would drive the price of electricity so low that renewables would be adopted much faster than we expect. Is your study consistent with that conclusion?

Heymi Bahran: A very good point.

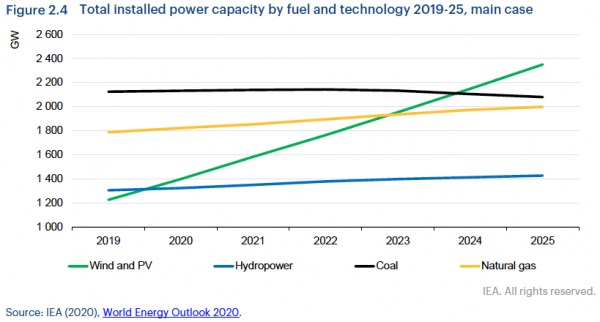

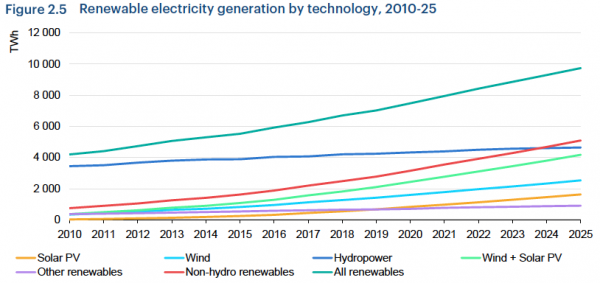

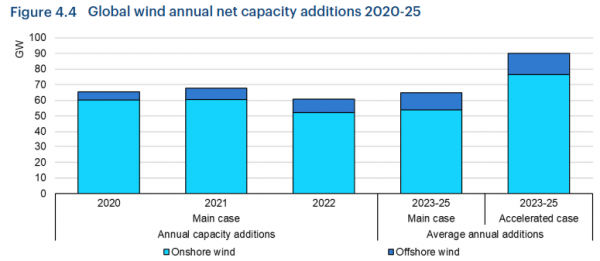

We expect solar PV capacity continue to increase over time in the coming five years. We also do two cases, main case and accelerated case. And it looks at the challenges that renewables face today, country by country in the main case, and then looks at how those challenges are met, if they are met, or what does the world may look like?

In our accelerated case, we see both wind and solar capacity to increase for solar view, we expect in both cases to grow as you indicate, however, we need to differentiate wind and solar here.

I think it’s an important point and why solar is much more in advantage than wind because globally wind plants, especially onshore wind plants. I’m sure it’s a problem in Canada as well. They are facing social acceptance issues because of their height because of how they are located. This is true everywhere in the world, and that’s why this affects delays in the construction problems in the permitting and so on and so forth.

Solar is the opposite side where there is no height. There is no basically size problem because you can install an off-grid in a mining facility in Canada, which is completely out of the grid, very small scale, but you can also include a 300, 400 megawatt scale projects.

So between those you attract incredible amount of investors, an incredible amount of sources of investment. That’s why solar PV is usually the more advantages and our numbers show that solar PV will almost grow double the size of wind, because of these facility.

Despite the fact that it’s not maybe cheapest option in many countries, investors can build solar PV plants much faster than wind plants today.

Markham Hislop: I was reading a Wood Mackenzie study on solar PV costs between now and 2030, and they were forecasting still a fairly significant drop in costs over the next decade. Is that consistent with what you found?

Heymi Bahran: Yes, very consistent. We see that solar PV costs in the next five years to decline by a quarter again and wind cost by about 10% to 15%. Obviously, continuous cost declines will make wind and solar more and more competitive. And already today, if you want to build a new electricity plant in the world in significant majority of the countries, you will see that wind and solar are cheaper. So that’s the first statement.

The second statement is that in more and more countries, it is becoming comparable to existing cost of fossil fuel generation. So which means that if you have costs about $30 per US dollars for solar PV generation wind generation, which we see these numbers around in the new contracts, this is equal to operating cost of coal plants in some countries. So we are entering into a new era I will say, where not only for new generation renewables are cheaper, but it’s slowly, it will be comparable and lower than existing generation.

Then you see a completely a different world.

Markham Hislop: Now Seba’s argument is that the cost of renewables, particularly solar combined with battery storage, which then makes it competitive with coal in terms of dispatchable power, potentially anyway, are we seeing that combination of wind and solar with batteries being competitive with existing generation now? Or is that something we’ll see in five years or 10 years

Heymi Bahran: Combined with batteries? Now that’s difficult to argue because with today’s costs but definitely if you take into account the historic development of battery cost reduction and solar PV cost reduction, obviously in the next 10 years. I don’t know exactly when and how you will very well see in some countries, this combination is cheaper than fossil fuel alternatives.

Markham Hislop: Does your analysis take into account the recent announcements by Tesla? For instance, Elon Musk had a battery day a month or two ago, talked about some of the engineering advances, such as dry coating of nodes that would drive down the cost and drive up the energy density of batteries, lithium ion batteries. And I think he was talking, you know, 2024, we’d see $57 a kilowatt hour, which is a tremendous decline.

Have you taken those kinds of calculations into account in your analysis?

Heymi Bahran: We do not forecast batteries in this report. So that’s the first point to make however batteries will play more and more role. And we do basic projections for batteries in the longterm.

But that’s why we are the forecast in this case looks at just renewables. And in some cases increasingly they will be combined with not only due to the scale, but also at a residential scale behind the meter in multiple countries. So we follow this trend, but overall, if you look at the overall renewables growth in wind and solar growth in the next five years batteries will be a small share of this because most of the plants in the world will be driven without battery storage facilities, including in the United States and Canada because currently battery costs does not allow today.

And the next two to three years, this kind of a big competitive advantage, batteries are growing mostly in places where there are subsidies such as Korea, such as Japan, such as some parts of the United States. So where you have also Australia, you have investment subsidies given to batteries. They grow there very fast currently though without the subsidies, the growth of the batteries is currently quite limited, I will say.

It will come definitely in the next five years,

Markham Hislop: We know that countries around the world are adopting a stricter climate policies, including carbon pricing. What role does that play in the adoption of wind and solar?

Heymi Bahran: So currently we looked at every single policy that drives the wind and solar project in the next five years in our forecast. We categorize the forecast by policy and obviously with the existing carbon pricing schemes the impact is very limited, either the price is too low or there are other policies that stimulate renewables much faster, such as auction schemes. For instance those that were implemented in Quebec at the time and in Ontario similar ones that those auctions that you open a competitive bid and you accept bids.

We expect that about 40% of the wind and solar growth will come from these auction schemes, which are not relevant to the carbon prices because it’s a separate policy. And we expect an increasing number of wind and solar plants growing outside of carbon pricing schemes, such as feeding tariffs auction.

We call them corporate PBAs, which means which means that companies are willing to buy renewable power and sign bilateral contracts. So this is an increasing trend that we will see, but also on top of that, we will see merchant plants, which are going to basically in the face of, in the face of the merchant plants, running on the wholesale electricity markets.

And also on top of that, we will see a combination of those sources where companies are bidding into an auction, some part of their output going to the spot market to raise other output and signed bilateral contracts. So this is very important to highlight in our analysis, shows that in the next five years, 15 to 20% of wind and solar will be outside of common policies, either these bilateral contracts, which shows the maturity of the industry, where the developers who like to take more risks, not to rely on policies. And this is obviously a game changer in the renewable world because it used to be on the line policies, but we expect more and more companies to be invest in renewables outside of this Commonwealth schemes, which is a good deal.

Markham Hislop: One of the areas I’ve been reporting upon and researching recently is electricity market reform. And that would seem to be consistent with the point that you’re making here. We’re seeing jurisdictions like Alberta in Canada, for instance, that has done pretty good work around that. And that will aid the adoption of wind and solar. And we’re seeing the same thing in the U S, what’s the electricity market situation outside of North America and are electricity markets being reformed and changed in response to the rapid adoption of renewables.

Heymi Bahran: This is a very, very good question. And you’re pointing to a very important issue. The second largest or third largest challenge that renewables will face in the next five years is good integration.

This is not a technical issue only. It’s also about how the market designs enable wind and solar to operate in a better way in an optimized way to the system. And you cited very good examples around in North America. Alberta did a very good job or last year by reducing the time in the spot market, which helps a lot for renewables.

The same thing happened in our Arcot. It’s 15-minute intervals that the market is running in Europe. We are seeing these kinds of developments very fast, but Europe is a bit lucky because all the countries are interconnected and the markets are single. So the products are completely aligned in, especially the balancing markets products.

So, which is very quick where this is happening in a slower extent, which we will see in the next five years, big reforms are happening in Japan. Very important in Korea, very important in China started some provinces which will be done at a national scale, hopefully in the coming five years also in India.

There are very small spot markets in the examples that I give, but we are going towards this direction to reflect in the markets value of the wind and solar.

We are not talking about any more levelized cost of energy – the comparison that I gave to you in your first question, if they are cheaper or not. Actually, this will become irrelevant in the coming years because we need to look at the value that brings into the system, which is a different calculation. And in order to extract this value, just to give you a very good example, if you have in the middle of the day, a huge solar energy coming in the value of that energy declines, because if there’s too much of it so we need to find products in the spot market in the wholesale market that reflects this new value.

This is a million dollar question in the world. So there are very good examples as you described to enable them to operate better.

But the examples of the reflecting, the real value, also the value of the storage is a million dollar question right now that everybody’s trying to find out because electricity markets are not designed that way. They’re designed on a marginal cost basis, rather than this kind of a renewable zero margin cost basis. I think we will see a lot of innovations on the regulation on market design in the coming years.

Markham Hislop: One of the questions I’m very curious about – I confess that is not showing up in my reporting so I don’t have even an informed opinion – and that is how countries whose economies are still developing and maybe Africa would be an example: whether they will do with electricity, what they did with telecommunications. Instead of building this complex infrastructure from the ground up or expanding what they have, and they’ll simply go into micro grids and virtual power plants and all sorts of other options that are lower costs because the technology enables it. What’s your take on that?

Heymi Bahran: This is a very good question. And we call this a question for years ago, whether Africa will leapfrog on this, on this. And it is, we see an incredible innovation in Africa in terms of first to replace or combine diesel generation with solar PV and batteries. So this is no brainer. There is no question about cost here.

The day that you will install solar PV and combine it with diesel generation, you start saving money from diesel. No question. And the return rate of this is two to three years in Africa. It’s quite simple.

Whether you will be able to find the money to invest in new solar PV plan, that’s the biggest question. So that’s a separate discussion. That’s the first thing that that is happening. So when there is availability of funds in Africa, we see diesel combined with solar PV in hospitals, in public buildings and so on and so forth in order to do that, that’s the first part.

Second part, there’s a huge business innovation on the off-grid sector, where there is no grid available, and the grid will probably not come to those areas. In those areas there is an incredible innovation of pay-as-you-go systems where you basically don’t pay anything for the investment and you pay while you use it. So this is a pure business innovation that is happening. So, which is very, very good.

The third one is industries where the mining sector in Africa, for instance, they already are using solar PV and combined with diesel which is an important development. The leapfrogging is happening on the off-grid side, but not only that, it’s also happening on the normal utility scale side. So Africa is building more wind than solar than anything that you can imagine.

Compare relative terms, obviously still, we are talking about very small numbers, but if you look at what they built, they mostly built, which is good, but we need to talk about the challenges. Obviously financing remains an important challenge and the planning of the grid is basically an extremely important factor because sometimes the investors will like to build a renewable microgrids, but they do not know whether the grid will come there in two, three years, then their investment will go sunk, obviously, right?

So we need to obviously take that into account these other regulatory problems.

Markham Hislop: Well, I’d like to expand on that issue, just a little bit, Heymi. When new technologies are adopted, we use the S-curve to explain how they get adopted over time. And one of the things we know is that as technologies drop in price and as they get a bigger and bigger market share, there are always obstacles to adoption that are non-cost related. And you mentioned some of the policies or you know, existing infrastructure sunk costs. There are all sorts of these of barriers to adoption that have to be overcome.

In your opinion, sort of looking at the global perspective, what might be the top three barriers to the adoption of more and more renewables?

Heymi Bahran: So if you look at the non-cost barriers, I will say the first and foremost, the most important challenge is policy uncertainty. We still see a lot of countries not providing a clear policy guideline, a clear regulatory guideline for renewables, for most wind and solar. So that is the first problem.

The second one is permitting and social acceptance. So how these permitting structures are established, and this is especially a big challenge for wind projects, especially onshore wind projects. And obviously the cost is not an issue anymore, but how we manage as a society the acceptance of these plants. And we cannot simply think about wind plants, as you can just not simply build them, whatever you want. You need a structure for that, and you need to inform the society and involve them in the decision making process. This is a big challenge that we see that is everywhere now, including in emerging countries, by the way.

So you see wind plants being delayed for years and years because of this because developers and government did not take that into account that it’s important to involve the community in advance of this. Canada actually has very good examples of is involving the communities in the beginning of the project level. This is the second largest one.

The third one is available finance. This is not cost related. It may sound cost related, but how the financing, especially emerging markets switch from investing in something else to renewables is a big question, a big challenge. And the question that we are working at the IAA, how we can promote and show that finance community, that this is actually an area that investment should go for the climate change and further reasons.

Markham Hislop: I think most of us will remember that in January BlackRock Inc.’s Larry Fink, CEO of the largest asset management company in the world, sent out a letter to CEOs and said that from here on out, climate risk is driving the allocation of capital. And it would seem like that that trend would favor wind and solar and renewables.

Do you think then that the larger trends that Fink was talking about will help to overcome some of these issues that you mentioned on the finance side?

Heymi Bahran: I think we are at the crossroads and the world is going as of this year more towards the renewable side. The example you gave is very important about the corporates wanting to invest more on renewables, but over the last, I will say three to four months, we saw a very large number of countries very large energy consumer countries, and announcing net zero targets. So these include China, Japan, Korea. We are talking and European union.

If you add those four together we are talking about a very important chunk of energy demand globally. This gives the policy movement. So we know where these countries would like to go. And on top of this, you have obviously a new US administration propose bills are also going towards that direction. We do not know obviously how they will implement it, those are uncertainties, but still, if you look at the direction of policy proposal of the new US administration, you see that they will go towards that direction too.

So if you had United States on top of this, you have basically the largest consumers in the pot of net-zero, which means the crossroads that I described is going slowly towards renewables.

And I think this will affect the financing community. And also over the last six months, we saw several banks announcing that they will stop financing coal in their portfolio, new coal, I will say. And this is also an important decision. I’m already world bank two years ago said that unless it is a critical for energy access or on a basis that they will assess they will not invest in finance coal plants in the world, which is a very important decision as well.

Markham Hislop: I’d like to get your response to some of the work that I’ve done. I’ve written a document called the energy declaration, I call it the optimistic and moderate vision for Canada’s energy future, but it applies outside of Canada. And my basic hypothesis is that the future is electric that somewhere down the road, mid 21st century or later, depending if you’re like Vaclav Smeal or not, the primary energy of the global economy will be electricity. What isn’t electric will be hydrogen or biofuels, something like that. The electricity provided by renewables will gradually supplant oil, gas, and coal. And the question now really is not, if it will happen, the question is when it will happen.

What’s your general response to my argument?

Heymi Bahran: So last year we had a slide that we put together and the title of that slide was, “The Future is Electric.” So it was totally in line with your previous reporting.

In 2019, only 20% of global energy consumption was from electricity. The rest was heat processes from industry and buildings or heat use, and the rest is transport. So when you look at the energy system, obviously there are easy to electrify sectors, and there are difficult electrify sectors.

But the timeframe that you gave, I will agree with you that there’ll be a lot of electrification happening. First of all, industrial processes, those that can be electrified will be electrified soon, especially with assets direct use of fossil fuel assets is getting aged in many countries, so they need to replace anyways.

The investors will ask the question, whether they should replace it with electric or direct use. So I think the efficiency that electricity provides is quite important to those processes in several cases. So I think those will be done, raw transport, definitely. I mean, this is a no-brainer already today that we see that will happen.

The question is that what are those difficult to electrify sectors like transport aviation, especially long haul aviation, where obviously hydrogen is being tested and can be used, but there are still many questions.

Where you cannot electrify some of the very energy-intensive sectors, we think that renewable waste can be used extensively in some of these sectors, especially the cement sector. We propose that the potential is amazing to use waste in cement and, but there will be a lot of different choices, but I will agree with your argument in the longer term that most of the things will be electrified. Those are not, hydrogen can be the vehicle. That will be done. Obviously, hydrogen produced from renewables.

Markham Hislop: Just final question now and again this is responding to something that is a part of my hypothesis: that the energy transition is driven now primarily by technology change.

Some people still argue that it’s all subsidized and driven by policy. It is not. That might’ve been true for the first two or three decades of the energy transition because when you have a pump that you want to get going, you have to prime it. And so the priming, it took place over two or three decades, but the priming is mostly done.

Now, the new energy technologies are lower costs. They have all sorts of value in other ways like less pollution and fewer GHG emissions, all of that. And that really it’s the accelerating pace of technology change that will be driving this forward.

And the metaphor that I use is that the energy transition is the bus and the climate policy is the accelerator pedal. If you want the bus to go faster, you press harder on the accelerator pedal.

What’s your take on that general view of technology driving the energy transition?

Heymi Bahran: So obviously the technology will be the main driver. But also the perception change, I think is very important.

So we did a little bit of research, this year’s report and show that oil majors are also entering into electricity field quite fast. Their installed renewable capacity, mostly wind and solar will increase by eightfold in just five years. So this is an important number that they are becoming, not an oil company, but an energy company per se. So that’s the first point.

The second point is that technological disruption is changing the way that many companies see the world. For instance, you see that many oil retailers are entering into the electric charging business in their portfolio, which is quite important.

I think and also many utilities are becoming energy service companies. So we see oil majors becoming energy companies, utilities becoming electricity service companies, which means combining two very important pieces of the transition. One is energy efficiency. The other one is renewables. So they combine these two and try to exploit the technology options and making a business case out of it. This is happening today at a slower pace.

I think I agree with you that this will basically increase very fast in order to make the transition happen. Faster and technology will be at the heart of this.

Markham Hislop: One final question, because I can’t, I can’t let you go without asking you. I’ve had experts over and over again. And I think this is absolutely right. The 2020s is the decade When many of these technologies hit their inflection point on the S curve. We are set for the 2020s to be the disruptive decade of the energy transition. And we will see rapid disruptive change between now and 2030. In fact, we’ll look back from 2030 on 2020 and marvel at how much has changed in just 10 years.

Would you agree with that?

Heymi Bahran: Agreed a hundred percent. No question. I agree. Definitely. This is 2020 to 2030 is critical for the energy transition change a hundred percent.

Be the first to comment