Rating: High school and post-secondary

Summary: Markham interviews Dr. Johannes Urpelainen about how China has become the leading financer of wind, solar, and other green energy projects. They also discuss China’s Belt and Road Initiative and why China continues to finance and operate coal power plants in developing countries around the world.

Related links:

Why the United States should compete with China in global clean energy finance

Markham Hislop: Welcome to another episode of Energi Talks, the podcast where we discuss global energy issues and trends with experts from around the world. In this episode, I’ll be talking to Dr. Johannes Urpelainen of the John Hopkins School of Advanced International Studies, where he’s the director and Prince Sultan bin Abdulaziz Professor of Energy, Resources and Environment, as well as the founding director of the Initiative for Sustainable Energy Policy. He’s written a Brookings Institute report entitled “Why the United States should compete with China in global clean energy finance.”

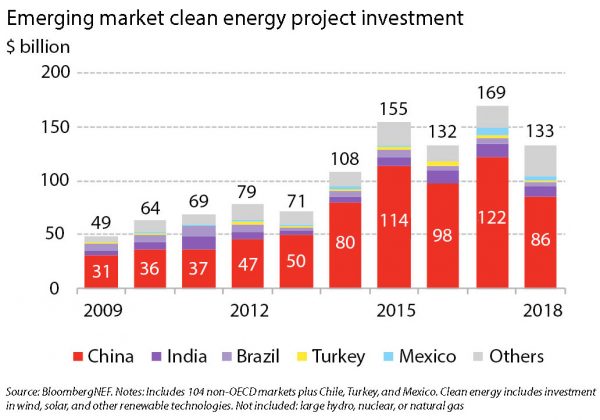

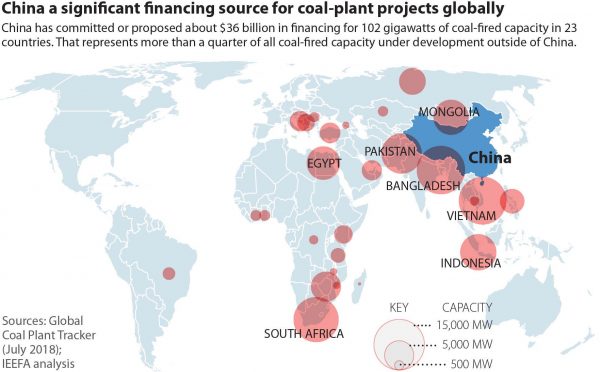

Now I’ll provide a little bit of context from your report. You say that China is the behemoth of global energy finance. Between 2007 and 2016, it financed a total of $197 billion in overseas energy sectors. And in fact, it is the biggest global financier in terms of foreign direct investment in electricity generation. Fossil fuel power plants with Chinese overseas, investment and finance currently produce approximately 314 million tons of CO2 emissions. So this is not an insignificant amount of emissions that are created, and of course, the trend is in the wrong direction because once these power plants are built, whether they be coal or natural gas, then those emissions are more than likely locked in for 30, 40, or 50 years, the life of the plant.

You argue that for a two-pronged strategy from the US in terms of both providing more finance to emerging countries, but also, and I found this very interesting, providing assistance to develop more robust regulatory environments in the emerging countries as well. That’s a very important part. So, with that background, maybe I’ll just get you to give us a brief overview of your report, please.

Johannes Urpelainen: As you just said, the idea of this report or brief was to look at what are some concrete steps that the United States can take to direct Chinese overseas energy finance to cleaner [energy] sources and possibly provide an alternative for countries in need.

There are very many countries around the world, especially in emerging Asia, that still have significant unmet energy needs. They need more power generation capacity. They need transportation fuels, they need industrial energy and a lot of the emissions growth today comes from those countries.

We already expecting China to peak in terms of greenhouse gas emissions in the next 10 years. The United States, Europe, Japan are all countries that are already in a declining trajectory. So if we really want to beat climate change and meet our targets of, let’s say limiting global warming below two degrees Celsius under the Paris agreement on climate change, we have to find solutions for South Asia.

In the report, we describe China’s leading role in global energy finance today, but then we highlight that much of that finance is really responding to demand from the recipient countries. It is not the case that China is pushing coal-fired power generation on countries that really don’t want it. It is rather the case that these countries are looking for energy solutions and coal-fired power generation is often the solution that they’re familiar with. The one that they expect to produce affordable and reliable electricity.

The Chinese companies, which do face a challenge in terms of decreasing domestic demand for their construction operation and finance, are then responding to those recipient countries needs and understanding this demand led logic is key because that creates an opportunity for the United States to go in and catalyze these clean energy markets with affordable finance strategies.

Markham Hislop: One of the examples that you provide is the China-Pakistan economic corridor. Pakistan approached China about building coal-fired power plants. They in fact proposed the development of at least 5,000 megawatts of new coal power plants and an investment of $20 billion. Is that a typical approach for emerging countries that are looking for Chinese investment?

Johannes Urpelainen: I would say yes and no.

Yes, in the sense that this is a typical situation of a country that faces a serious energy deficit. Just 10 years ago, Pakistan’s ability to generate electricity for industry, air conditioning, and commerce was very limited and they were really looking for solutions. China was a natural choice because China and Pakistan have a longstanding relationship. Pakistan really needs kind of a major power on its side because it is in a continuing conflict with India, which is a much larger country with nuclear weapons and all that.

The typical story here is that the country had an energy deficit and they did not really see any other alternatives at that point. Coal was the primary kind of natural, easy, understandable solution for them.

What is atypical here is that because Pakistan has such a strong relationship with China, they also had the geopolitics working in their favour. They could call China and say, “Look, we’ve been your loyal ally for a long time, we need finance. Could you please provide some?” Other countries, don’t have the same geopolitical cachet with China.

Markham Hislop: Could you give us an example of other Asian countries that are a little bit more typical, maybe Vietnam or a country like that?

Johannes Urpelainen: I would say that Indonesia is an interesting case here. Indonesia has a very large coal sector that has historically played a very large role in the economy, everything from mining to power generation to industrial uses. Chinese companies have played a major role in construction. There’s also Chinese finance in the Indonesian coal sector.

And this is atypical, Indonesia is kind of in a carbon lock-in. They’ve been doing coal for such a long time that they don’t really know what else to do. But they don’t have a geopolitical relationship with China. In fact, Indonesia is in kind of an awkward position because they’re trying to maintain their relationship with the United States and Japan, which China perceives as competitors.

Markham Hislop: In a case like this, you make the point that if the host country is looking for investment, comes to China and says, “we’re not interested in coal power this time, we would like to do some renewable, some wind, some solar or whatever it might be. And can you help us with that?” China’s quite happy to do that?

Johannes Urpelainen: Yes. Certainly, China has itself a large renewable energy sector. In fact, domestic capacity expansion in renewables is now in the hundreds of gigabytes in China. There are many companies that could do an outstanding job building renewable energy capacity.

The one caveat to this is that if you look at China’s ability and willingness to operate those plants, instead of just doing the construction, but actually take an equity position and run the plants in Pakistan or Indonesia, that is much more limited because there’s geopolitical risk. There’s just sovereign, default risk, there’s all kinds of challenges.

The host countries do face a challenge in the sense that they might not have the domestic companies that would then run the plants that the Chinese have built.

Markham Hislop: You make another point that the Chinese industry is currently oversupplied, and I’m talking about the renewable, manufacturing industry, wind turbines and solar panels and so on. Their domestic demand has contracted, and they’re looking to these developing countries as an outlet for their surplus capacity. How big a pressure is that on the Chinese policy?

Johannes Urpelainen: This is a very significant pressure and challenge in China.

China has historically grown into an economic superpower with industry and manufacturing. It really is the world’s factory. And if you look at what’s happening during COVID-19, China’s position in global markets, if anything is stronger than it used to be. But it also means that there’s a lot of industrial overcapacity in construction, power plants, factories because China now has all that infrastructure. It doesn’t need more of that.

China needs more tech, China needs more services, more innovation, but at the same time, there are so many jobs. There’s so much capital deployed in these companies that there are pretty desperate and looking for opportunities, whether it’s building power plants within China, that nobody needs, this is still happening. They’re still building coal-fired power plants, despite the huge overcapacity in power generation within China. Or it is global markets. They’re looking for opportunities to build.

My only wrinkle or change to the conventional narrative is that the Chinese would be very happy to build solar power plants, wind power plants, geothermal, hydro, if that’s what the recipient countries are looking for.

Markham Hislop: Now, we generally tend to think of the Chinese sphere of influence as within Asia. But you note here that in Latin America, Chinese investors have financed wind power projects where the total generation of just over 4,000 megawatts. That’s actually a significant investment.

Johannes Urpelainen: That is correct. China has over the past 20 years built significant relationships with many Latin American countries. And I think it all started in the early two thousands when China was very worried about access to natural resources and resource security and energy security, it made a lot of sense then to work with countries like Bolivia that have a lot of natural resources.

That created these markets and openings for Chinese companies in an area that’s traditionally been dominated mostly by the United States.

Markham Hislop: Let’s talk about something that I perceive as being a push driven, as opposed to the pull of demand, and that’s China’s Belt and Road Initiative. So you note that of the 56 Belt and Road Initiative countries between 2014 and 2017, most of the Chinese energy financing and investment were in carbon-intensive sectors.

Johannes Urpelainen: That is correct. So the Belt and Road Initiative does play an important role here, but our research at the Initiative for Sustainable Energy Policy, with my collaborator Chuyu Liu and with professor Tom Hale from Oxford University, found that The Belt and Road really has this bottom up logic.

Chinese companies are looking for opportunities in the global markets when they go to the Chinese policy banks, which are funding and financing these projects. They tend to frame the projects as Belt and Road because that gives them some political capital and recognition given that China’s premier Xi Jinping was the one who kind of branded this Belt and Road.

Belt and Road is an important push, but in our assessment, some people historically have kind of over-estimated the strategic dimension of Belt and Road. It is equally domestic, rent-seeking, an opportunistic activity in China and outside China.

Markham Hislop: Now your recommendations for what the United States should do in response to China comes at a very opportune time. Next week, we’ll see President-elect Joe Biden’s inauguration. He has committed $2 trillion over 10 years to his climate and clean energy plan. And in reading his plan, one of the things that stuck out for me was his commitment to elevating the United States as a clean energy superpower that will compete directly with China. And so you have a two-pronged strategy here. Maybe you could describe that for us.

Johannes Urpelainen: Absolutely. First of all, I would agree with the view that President-elect Biden’s plan gives the US a natural opportunity to actually act on some of these recommendations. And so what we propose is a twofold strategy.

On the one hand, it is important to directly compete with China on clean energy finance. That means going out to these countries and providing finance for clean energy. If these countries need energy, the United States should go in and offer loans or for other kinds of financial mechanisms and deals at affordable interest rates so it makes sense for these countries to participate and cooperate with the United States.

This could be done, for example, through the New Development Finance (DFC) Corporation, which is in a fantastic position because it has a much greater ability to offer finance than the previous one, The Overseas Private Investment Corporation, had. The DFC can offer $60 billion of funding on top of finance.

The other thing that we observed in our research is that many of these recipient countries really struggle with mechanisms like environmental impact assessment, regulation, monitoring, and enforcement of rules. And given that what we know about the environmental impact of fossil fuels, just strengthening these rules and engaging in technical cooperation with countries like Pakistan and Indonesia would naturally make clean energy much more competitive because the environmental footprint is so much smaller than that of fossil fuels.

Markham Hislop: You make the point in the article that one of the advantages of taking this approach is that the United States can help to grow clean energy markets in these emerging countries whereas now they may be non-existent or they may be very immature, but the United States can help them to build those out. And then that then creates increasing demand for clean energy. Have I got that correct?

Johannes Urpelainen: Absolutely. So one of the key things to note here is that globally renewable energy is already very affordable. In fact, if you want to generate a kilowatt-hour of electricity today with wind or solar, it is significantly cheaper than a kilowatt-hour of new coal-fired power generation.

But the challenge is that some of these countries have not yet climbed the learning curve. They don’t yet have the expertise, the experience, to do this.

If you take a country like Vietnam just a few years ago, it looked pretty hopeless. The renewable energy market was very small. Nobody was doing deals, there wasn’t a lot of enthusiasm. And just look at where they are today. Today they are really skyrocketing. They are investing so much in renewables, whether it’s rooftop, large-watt solar or wind onshore, soon maybe offshore, it is really exciting.

So, if the United States can help build this kind of momentum in Indonesia in Pakistan, that could be a game changer.

Markham Hislop: And I think there are lessons for what’s going on in Canada and the US for these countries because we see that the role of regulation and the role of markets for renewable energy is really important. California’s blackouts in the summer of 2020 shows us what happens when regulation is maybe inadequate. We are seeing US utilities and, to some extent, Canadian utilities, grappling with this whole challenge of distributed energy.

How are you going to design markets that can incorporate that? And then there are all of these new technologies that create challenges but also opportunities for utilities to provide services and other revenue generating components of renewable energy.

So if sophisticated economies like the United States are grappling with this, we can only imagine what emerging countries – which may dominated by coal and they don’t have the technical expertise, they don’t have the experience – how much more difficult it would be for them.

Johannes Urpelainen: That’s a great point.

India is actually a really good example of this at the very early stages of renewable energy development. The challenge is just to build as much as you can. It’s all about capacity addition. That includes its own challenges, but they are not that different from the fossil fuels. These countries have found ways to do this. And India, for example, has really driven down the cost of wind and solar power dramatically over a short period of time.

But once you reach a point where a significant percentage of your electricity comes from the so-called intermittent, renewables, solar, and wind power, then you need regulatory capacity. You need dynamic pricing, you might need some battery storage. You need ways to provide electricity when the sun doesn’t shine and the wind doesn’t blow. All this can be done, but it does require quite a bit of expertise and learning by doing.

That’s why it’s so important that these countries don’t repeat the mistakes that the wealthier countries have made, but this kind of cross-country learning is possible,

Markham Hislop: Taking a broader perspective for a moment, I often see in discussions around renewable energy that once the cost of wind and solar are below existing coal and natural gas, as they appear now to be, that the transition to renewables will be relatively painless. We’ll just take out the fossil fuels and plug in the renewables and everything will be much better, and we’ll be on our way to net zero emissions.

But this discussion, I think, illustrates just how complex the transition issue is. It’s finance, it’s technology, it’s regulation, and you need to get it right. If you get it wrong, as California has, you see what the consequences are. Of course, politicians and regulators worry about those sorts of things, which is kind of an impediment to adoption in a way.

Would you agree with me that this illustrates some of the complexity of our transition off fossil fuels into clean electricity?

Johannes Urpelainen: Absolutely. So if we think about the way we measure the cost of solar power generation, we typically measure it at a time when the conditions are good, the sun is shining, but if you are in almost any country – except maybe my home country, Finland, in the summer and it’s 9 PM at night [and the sun is still shining] – there is no sunshine. You are not going to be generating any electricity at that time with solar power. Where is that going to come from?

By the way, countries like India and Pakistan tend to have peak electricity demand late at night, because that’s when people are at home, having their dinners, running the air conditioning and all that.

It’s a real challenge. I do think we are learning and it’s pretty incredible how much progress we’ve made over 2020. This is the first time in my career as an energy and environmental scholar that I really have difficulty keeping up with all the progress, but still the challenge is significant and we should not underestimate it.

Markham Hislop: This has been a fascinating discussion, Johannes. Any final thoughts on what the United States should be doing under the new Biden administration in terms of positioning itself as a competitor to China on global energy finance?

Johannes Urpelainen: I think we have a situation here where, on the one hand, the United States will come into 2021 with a lot of newfound goodwill because there are not that many countries out there that prefer President Trump to President Biden and the ones that do, don’t have a lot of interest in dealing with climate change. The United States has a real opportunity now to build coalitions and claim back some of that momentum that the United States had during the Obama administration.

At the same time, the United States has broken so many promises and been such a flip-flop over the past 10, 15 years, 20 years in climate policy, that it’s important to also stay humble. And instead of telling other countries what to do, show a good example, reduce emissions, and then work with other countries once you’ve demonstrated that you can really do it at all.

So, a combination of leading by example, and then supporting some of these key emerging countries in a way that’s co-operative, and not in any way based on sanctions or pressure or threats, I think would be the right way to go.

Markham Hislop: A final thought here, Johannes and that is that there’s a lot of discussion in the United States about energy jobs. And it seems to me that the US taking this approach that you advocate would create a significant demand on the American side for expertise, in financing, in technology. There’ll be new manufacturing jobs created to help service these projects that might go on in Asia or Latin America, wherever they might be. So not only would this be a case of the United States competing with China in terms of global energy finance, but it seems to me that the economic benefits to the United States would really be quite considerable.

Johannes Urpelainen: Absolutely. I think it’s very clear by now that there’s a huge amount of work that can be done, a huge wide range of emissions reductions that can be achieved with net-positive benefits for the society and the economy. In my program, we train graduate students who become energy professionals. Huge demand for this right now. It’s a booming economy, and we just launched a new degree called master of arts in sustainable energy because there was just so much demand. So this is definitely a future area for economic growth, innovation and employment in the United States and Canada.

Be the first to comment