Electric cars are expensive, have limited range, and generally provide low value compared to gasoline-powered vehicles

This spring the Canadian government announced that a zero-emission vehicles policy would soon be forthcoming, but is this a good use of the limited resources Canada has to reduce its greenhouse gas emissions? Absolutely not. Electric cars still provide very poor value for Canadian consumers – who have adopted at lower rates than other developed countries – and that isn’t likely to change for another 10 to 15 years.

A go slow approach flies in the face of a blizzard of media hype EVs are have enjoyed for a few years now. There are all manner of forecasters – Tony Seba of Stanford, Bloomberg New Energy Finance, Prof. Ray Mills of Australia – who have plugged data into their spreadsheets and now predict hockey stick growth in EV sales.

Seba thinks 95 per cent of miles traveled in the United States in 2030 will be by autonomous EVs and Americans will have given up on private car ownership in favour of Transportation as a Service.

Bloomberg is so giddy about the prospects for EVs that the consultancy upgrades forecasts almost weekly.

And Mills forecasts that by 2040, 100 per cent of the global auto fleet will be EVs. That’s an increase of 99 per cent, in case you were wondering.

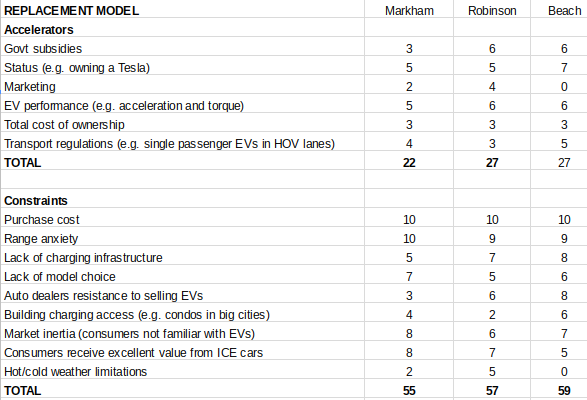

They’re wrong for a multitude of reasons. In my model, the rate of adoption is determined by the balance of accelerators (those things that speed up adoption) and constraints (those things that slow down adoption). If the constraints significantly outweigh the accelerators, expect adoption (i.e. sales) to be slow.

To measure the relative strength of accelerators and constraints, I developed a survey with the help of Dr. Fred Beach, executive director of The Energy Institute, University of Texas at Austin, and Chris Robinson, EV analyst for Lux Research in Boston, Mass.

The three of us assigned values from 1 (least strong) to 10 (most strong) for all the accelerators and constraints we thought were relevant.

As the chart demonstrates, the constraints are more than twice as powerful as the accelerators. Hence, my hypothesis that adoption of EVs will continue to rise, but not nearly as rapidly as EV boosters think.

The data support my argument.

Last year, 88.1 million automobiles were purchased worldwide, of which 775,000 were EVs. That’s less than one per cent of global sales. EVs are a percentage of the global light duty vehicle fleet are just .02 per cent (2 million EVs, 1 billion cars and trucks).

According to the Inside EVs website, this year 893,370 EVs were bought in the first 11 months and sales appear to be headed for just over one million, growing the global fleet to three million.

That leaves just 17 years to reach the IEA’s forecast of 100 million EVs on the road by 2030. Could automakers even churn out 97 million EVs in that time? Unlikely.

That leaves just 17 years to reach the IEA’s forecast of 100 million EVs on the road by 2030. Could automakers even churn out 97 million EVs in that time? Unlikely.

So, why aren’t consumers buying more EVs? In a word, poor value.

To illustrate the point, let’s use the fancy new Tesla Model 3, which began rolling off the assembly line only a few months ago but has already been hailed as the internal combustion engine killer. More than 400,000 buyers plonked down a $1,000 deposit on a $35,000USD car with a 200 mile (320 kms) range.

Let’s be generous and assume that our hypothetical Model 3 buyers will qualify for the $7,500 US federal EV subsidy and some may also get a $2,500 state grant, bringing the cost down to $25,000USD (Ontario and Quebec have generous EV subsidies, BC’s is $5,000 and Alberta doesn’t yet have one).

That’s roughly the price of a well equipped Toyota Camry, a car with a strong reputation for reliability and value. As a long-time Toyota owner, I can tell you from experience the company makes an excellent “transportation appliance” that is economical to operate and maintain, usually staying on the road long after lesser makes have met the crusher.

What does the Model 3 do better than the Camry?

If we’re being honest, not much. The Model 3 does pretty much what the Camry does, just with a different fuel (electricity instead of gasoline).

The Model 3 will be peppier, especially if Tesla includes the aptly named Ludicrous Mode that made the four-door Model S the fastest production car in the world. But Ludicrous Mode hasn’t done much for Model S sales, which are on pace to be slightly lower than 2016.

The Model 3 may also have a lower “total cost of ownership” over its lifetime because it will require less maintenance and repairs. But consumers don’t buy cars that way. They generally get the most car their monthly transportation budget will permit. Repairs five or 10 years down the road will be a problem for the second or third owners, not them.

The survey provides a clue to the two biggest constraints after price: poor range and a paucity of models to choose from.

Automakers are slowly remedying those issues. GM announced last month that in 2021 it will introduce a fleet of EVs with more model choice, lower prices, and longer ranges. Other manufacturers will no doubt rush to keep pace in the global race to dominate the new electric vehicle industry.

But CEO Mary Barra is forecasting sales of only one million units per year by 2026 for General Motors.

If we assume GM will among the industry leaders, there simply aren’t enough EV manufacturers ramping up production fast enough to meet the IEA 100 million EV fleet by 2030.

A modest 10 million to 20 million seems more likely.

And keep in mind that the total global auto fleet is expected to double to two billion by 2040.

I’ve written elsewhere about the three disruptions that could rapidly increase EV adoption: 1) introduction of super-batteries; 2) the spread of Seba’s Transportation as a Service business model; 3) Chinese manufactures EVs in volume and drives down prices just as it did for solar panels over the past decade.

Each of those disruptions promises to significantly increase value for consumers. All three occurring at the same time could provide a huge boost to EV sales.

But even if all three of those disruptions happen, they are all in their infancy and aren’t likely to gain much traction until the mid to late-2020s, perhaps not even until 2035.

If this hypothesis is true, then why would Canada want to heavily subsidize immature technology Canadian consumers have little interest in? Why not wait 10 or 15 years until EVs offer more value and sales are ready to take off?

There is no shortage of other sectors – such as industrial processes or building energy efficiency – where a dollar invested by government in more mature technologies would provide greater reductions in GHG emissions.

If the Canadian government is set upon subsidizing EVs, then why not focus on work electric vehicles, where there appears to be demonstrable value to early adopters?

At the very least, Ottawa should slow down what appears to be a headlong rush to embrace a trendy idea and seriously consider the assumption, common among clean energy boosters, that electrifying passenger vehicles is good policy.

It may be in the future, but it isn’t today.

Holding our governments to account for the cost & value of reductions is needed.

Spending with poor returns is a waste regardless of the intiatives popularity. Benchmarking costs against the carbon reduction should be mandatory disclosure. Spending above $50/tonne of reduction should be visible & called out.

Good reporting and incisive commentary as usual, Markham.

Same thing as they said about solar PV 15 years ago: “Why subsidise something that is not ‘cost-effective’.” Oh, I see, only when something becomes economically viable could it be subsidised… !

The accelerators and constraints analysis is very interesting and is very worthy of doing once a year. It seems that there is some bias built into the subjects listed as constraints though, as some of those categories are overlapping.

It would be worth extrapolating this analysis to 5 years from now and seeing what the results are… because many of the answers to that analysis are as a result of economics and policies over the last 5 years and so aren’t looking at the future — even though the analysis comments on the future.