US imports 5.5 Bcf/d of Canadian natural gas, expected to decline to ~5 Bcf/d (almost 10%) starting in 2019

Construction of more natural gas pipelines in northeast United States is bad news for Western Canadian producers as the prolific and low-cost Marcellus and Utica formations in Pennsylvania and Ohio displace higher cost Canadian gas, according to analysts Drillinginfo.

Traditionally, Northeast gas demand has been met by producers in the Southeast/Gulf of Mexico, Midcontinent, and Canada.

Production in the Marcellus and Utica has risen sharply over the past ten years and now represents 35 per cent of total dry gas production in the United States.

“With the Northeast bottlenecks getting relieved later this year, regional pricing will improve and this will benefit Northeast producers, so their netbacks will increase,” said Maria Sanchez, manager of energy analytics at Drillinginfo and lead author of firm’s quarterly market outlook report.

“For Canada this means that their market price will also be higher.”

Sanchez cautions that since many of the new pipelines are targeting the Midwest market, Canadian gas will have to compete with Northeast gas from the Marcellus and Utica.

Sanchez cautions that since many of the new pipelines are targeting the Midwest market, Canadian gas will have to compete with Northeast gas from the Marcellus and Utica.

“Canada gas is expected to get pushed back into the Midwest as Rover and Nexus come online, therefore losing market share,” Sanchez said in an email.

“However, US imports from Canada are not expected to be 100% displaced as the West and Northeast premium markets still need Canadian gas to meet their seasonal needs.”

The US currently imports an average of 5.5 Bcf/d of natural gas from Canada and Drillinginfo expects this to decline to ~5 Bcf/d or almost 10 per cent starting in 2019.

In Northeast Gas Midstream, Drillinginfo points to anticipated pipeline capacity constraints to end in 2018, when key takeaway projects will come online and add over 5 Bcf/d of additional Northeast pipeline takeaway capacity. Energy Transfer Rover Phase 2, Transco’s Atlantic Sunrise, Nexus Gas Transmission, and Columbia’s Gulf Xpress projects will, in effect, debottleneck the region during the third quarter.

Regional gas basis is therefore expected to trade within variable transport costs of about $0.20–$0.30 per MMBtu below Henry Hub.

If pipelines like Constitution [210 kms pipeline carrying 650 million cubic feet per day from the Marcellus to New York] and Northern Access [155 kms pipeline carrying 490 million cubic feet per day from Pennsylvania to New York and Canada] go forward, get over all their regulatory issues, Sanchez expects additional declines in US imports from Canada.

“This rapid and immense growth in the Marcellus-Utica has created tremendous challenges for natural gas producers over the past ten years, the most significant being bottlenecked pipeline takeaway capacity,” said Sanchez.

“That bottleneck has caused gas prices to drop in the region. Pipeline infrastructure operators have responded by changing flow direction in existing pipelines and expanding capacity. However, those capacity additions haven’t kept up with production growth, and basis has remained depressed — thus far.”

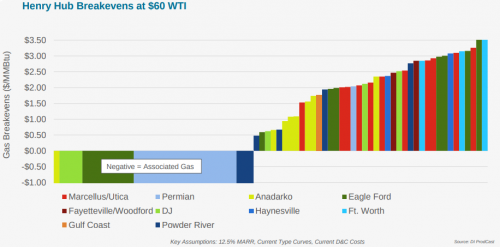

Based on Drillinginfo’s pricing expectations of Henry trading somewhere between $2.65 and $2.75 MMBtu over the next five years, by 2021, production in the Northeast will reach almost 30 Bcf/d, an increase of more than 5 Bcf/d from current levels.

Natural gas production in the Marcellus and Utica basins has risen from about 2 Bcf/d in 2008 to more than 26 Bcf/d as of February 2018. While other basins also experienced growth during the same time period, the rates have been much lower, such as the Eagle Ford at 3.3 Bcf/d, Permian Basin at 3.2 Bcf/d, and Anadarko Basin at just 1.2 Bcf/d.

Be the first to comment