This article was published by Wood Mackenzie on Nov. 20, 2023.

Chinese companies have made significant strides in the Belt & Road (B&R) initiative’s overseas power projects over the past decade. With an estimated investment value of around US$200 billion, over 300 projects have installed 128 GW of power, equivalent to 1.3 times Australia’s installed capacity in 2022.

However, challenges have emerged, leading to the cancellation or shelving* of over 20 per cent of projects to date, according to Wood Mackenzie’s report ‘Belt & Road at 10: powering on through growing pains.’

The report highlights the significant achievements and challenges Chinese firms encountered in overseas power projects in the first decade of China’s Belt & Road Initiative (BRI).

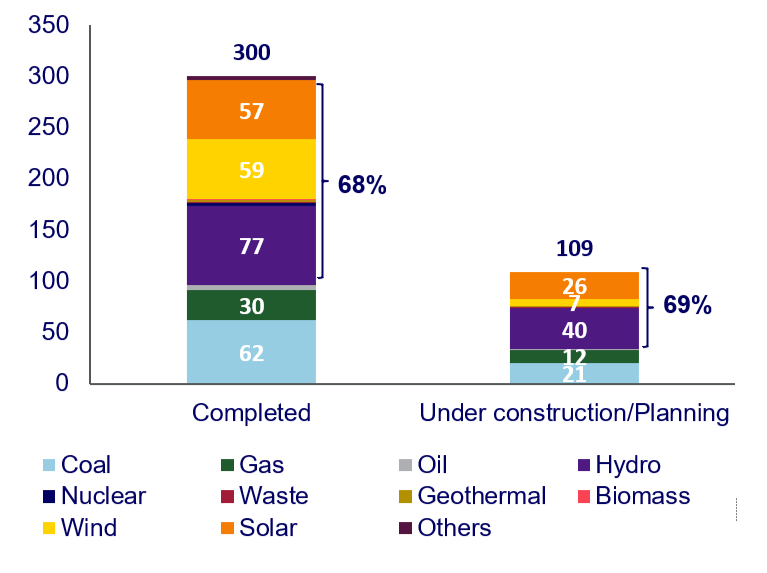

Asia has emerged as the primary destination for BRI power projects, accounting for 75 per cent of the total capacity. Among the completed projects, 62 coal and 30 gas power projects represent 57 per cent of the total BRI project capacity. Additionally, 199 renewable** projects, including wind, solar, and hydro, have been completed, contributing to 68 per cent of projects and 37 per cent of capacity. The remaining 6 per cent of the capacity is from nuclear and other sources. The share of renewables in newbuild capacity has increased significantly from 19 per cent ten years ago to 47 per cent in 2022.

Completed and future projects in terms of project amount

According to Wood Mackenzie’s findings, Pakistan, Vietnam, and Indonesia are the top three markets of BRI power projects out of a total of 72 countries. The top 15 markets totalled 103 GW, representing 80 per cent of all completed projects.

Alex Whitworth, Vice President, Head of Asia Pacific Power and Renewables research at Wood Mackenzie, said, “despite making progress, Chinese companies have faced significant challenges, particularly in developing markets. Of the 481 BRI projects that Wood Mackenzie monitored, 72 were either cancelled or put on hold after initiating them. Most affected projects were in Asia and Africa, with Asia contributing 60 per cent and Africa contributing 32 per cent of the total capacity.”

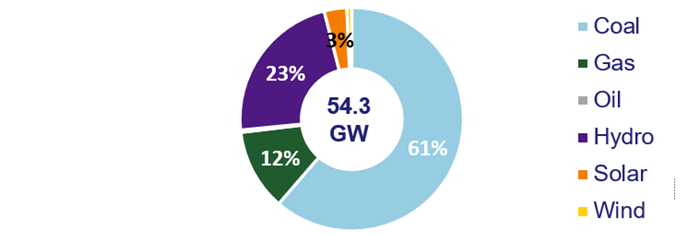

The cancelled or shelved projects had a capacity of 54 GW, which included 33 GW of coal, 12 GW of hydro, 6 GW of gas, 2 GW of solar, and 0.4 GW of wind. Coal power projects were the most affected, primarily due to changes in policy and increased political pressure to reduce carbon emissions. China’s ‘No new overseas coal power’ policy, announced in September 2021, has had a significant impact on the BRI project pipeline.

Share of technology in terms of project capacity by 2023

Renewable projects also faced challenges, with 33 projects being cancelled or shelved, primarily due to commercial risks such as cost inflation and over-optimistic financial assumptions. Solar projects accounted for 70 per centof the impacted renewable projects.

“The most common factors that led to the failure of overseas projects were the changes in policy and cost. Chinese companies faced more risks when developing greenfield projects, with a 27 per centrate of cancellation or shelving, compared to a 9 per cent failure rate for pure EPC (engineering, procurement, and construction) turnkey projects,” Whitworth added.

However, despite the challenges in policy towards coal and unstable environment, the outlook for Chinese overseas BRI power projects remains steady, with a pipeline of projects estimated at about 13 GW per year, and large potential upside for wind and solar. Renewables projects are a growing focus and account for 57 per cent of 80 GW of planned capacity. Asia and Africa will remain the top two markets, accounting for 93 per cent of the future projects.

“The BRI’s influence on power markets is set to grow, with a further 80 GW already under construction or at the planning stage. China is changing its overall strategy, so we expect to see more focus on renewables, and more direct investment than the bilateral lending that was more common in the early years of the BRI,” Whitworth concluded.

*Renewables include hydro, nuclear, waste, geothermal, biomass, wind and solar.

**‘Cancelled or postponed projects’ refers to projects with existing contracts but have been cancelled or shelved.

Be the first to comment