A recent report by ‘Wood Mackenzie Zinc Markets Service’ warns that efforts to decarbonize the steel industry through adopting Direct Reduced Iron Plant (DRI) production with green hydrogen could have significant implications for the circularity of zinc. The shift towards the use of more DRI in electric arc furnaces (EAF) versus scrap steel is expected to increase the cost and carbon intensity of zinc recovery due to the reduced zinc content in EAF dust.

Wood Mackenzie’s report estimates that the current EAF process generates approximately 535 million tonnes of steel per annum, resulting in steel dust containing anywhere from 0.2 to 3.4 million tonnes of zinc annually. Raw materials analysis reveals that around 1.6 million tonnes of zinc units are sourced globally per year from the zinc in steel dusts and other residues, indicating an average zinc content of 17 per cent in EAF dust. More use of DRI in the EAF process will lead to a decrease in zinc rich dust, further increasing the cost and carbon intensity of zinc recovery.

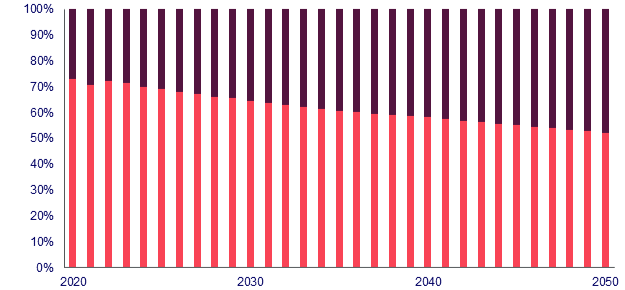

“By 2050, nearly half of the world’s steel production is projected to be through the EAF route. This transition is necessary for decarbonization efforts, but it poses challenges for the zinc industry in meeting the demands of decarbonization and the circular economy,” said Andrew Thomas, Head of Zinc Markets at Wood Mackenzie.

Basic Oxygen Furnace (BOF), Electric Arc Furnaces (EAF)

Source: Wood Mackenzie Steel Markets Service

The current “best available technology” for zinc recycling is highly carbon-intensive, making it difficult for the zinc market to align with decarbonization goals of the steel industry. According to Wood Mackenzie, primary smelters currently utilize up to 25 per cent of zinc oxides and other residues in their raw material feed. However, this practice also poses a challenge for the future of secondary zinc. The primary raw material for smelters is zinc oxide, obtained through the pyrometallurgical process of recovering zinc from steel dust. Steelmakers either have to pay for its disposal in specialized landfill sites or hand it over for further processing.

“Alternative methods of recovering zinc from steel dusts have proven unsuccessful, posing a risk that the steel industry’s decarbonization efforts and rising carbon costs could inadvertently hinder the circularity of zinc. This could result in a higher amount of zinc being lost if steel dust is used in the production of ferro concrete and potentially fertilizers, thus preventing the recovery of zinc altogether and represents a significant challenge for the zinc industry in meeting the demands of decarbonization and the circular economy” Thomas added.

Editor’s Notes:

The findings summarised in this news release are taken from Wood Mackenzie’s ‘A challenging future for secondary zinc’ report.

Be the first to comment