By Michael Waldron, Lucila Arboleya

This article was published by the International Energy Agency on Nov. 1, 2019.

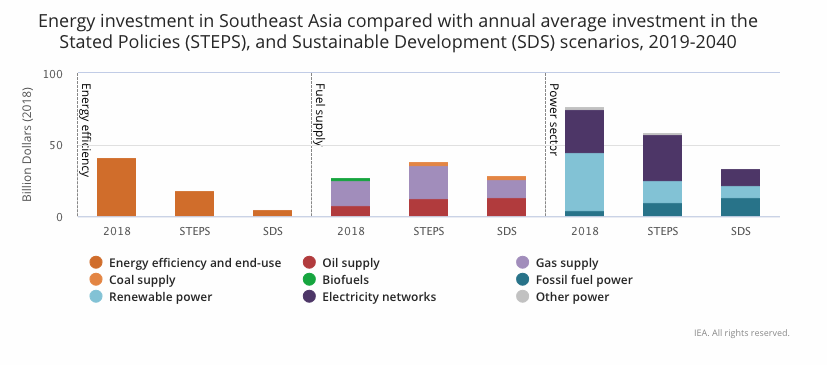

The financing gaps and opportunities differ starkly by scenario. Under today’s policy settings, the region’s investment needs over the next two decades total $2.5 trillion while under a more sustainable pathway (i.e. consistent with the Paris Agreement) they rise to near $3.3 trillion.

Sizeable reallocation of capital from fuels towards power and efficiency will be needed, particularly under a sustainable pathway, where renewables spending quadruples.

Bridging investment gaps with more private finance

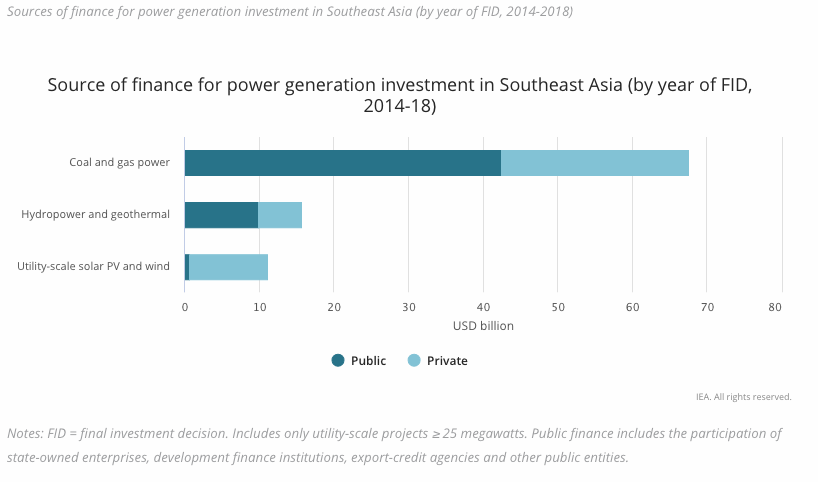

The energy investment situation is most acute in the power sector, where a number of systems are under financial strain. To date, public actors – including state-owned enterprises and public financial institutions – have provided the bulk of funding, particularly in thermal generation. By contrast, wind and solar PV projects have relied much more on private finance, spurred by specific policy incentives. In addition, funding for over three-quarters of generation investment has come from within the region. This landscape reflects prevailing decision-making frameworks, which have revolved around state-owned utilities and the distortionary impact of energy subsidies.

Public and regional sources alone cannot cover the sizeable investment needs ahead. Sustained and balanced access to international and domestic sources of private finance, complemented by limited public sources, would better help Southeast Asia fund its energy goals. This requires reforms and greater policy focus on tackling the risks facing investments, especially in renewables, flexibility assets and efficiency. With the dramatically improved economics of renewables in many parts of the world, the region now has a window of opportunity to transform its investment environment. The Outlook points to efforts needed across four priority areas, while recognizing that market conditions and underlying risks differ starkly by country:

- enhancing the financial sustainability of the region’s utilities;

- improving procurement frameworks and contracting mechanisms, especially for renewables;

- creating a supportive financial system that brings in a range of financing sources and

- promoting integrated approaches that take the demand-side into account.

Priority 1: Enhancing the financial sustainability of the region’s utilities

The region’s utilities, mostly state-owned, function as the primary counterparty to private generators and are the main investors across the power sector. Their financial sustainability depends on their ability to recover costs, which is influenced by customer connections, operational performance and regulatory frameworks. Cost-recovery varies across Southeast Asia markets, with particular challenges related to setting retail tariffs in a way that balances system needs and affordability for consumers. For example, despite improved borrowing conditions for Vietnam Electricity (EVN), financial performance is tenuous and tied to government decisions on electricity prices, which remain low by international standards. By contrast, in Malaysia, a combination of improved operations, better financing and regulations for cost-pass-through supports a relatively high level of per capita investment for grids.

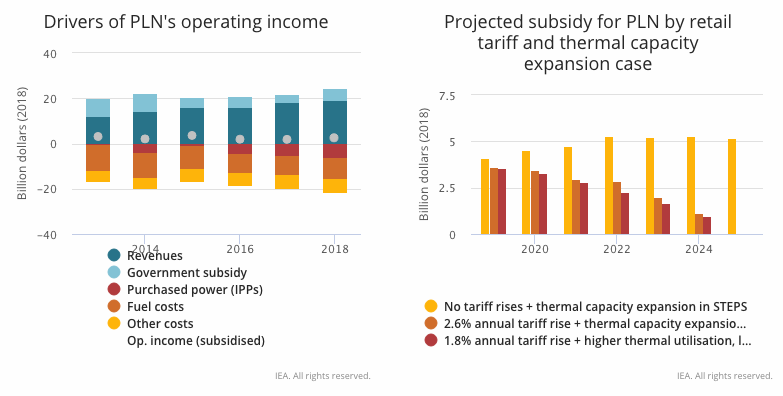

Underperformance can put pressure on government budgets, as in the case of Indonesia. Following several years of improvement, increased financial pressure on PLN, due to rising power purchase and fuel costs in the face of frozen retail tariffs, prompted a year-on-year boost in government subsidies in 2018 (equivalent to 3.2% of total state spending). Looking ahead, PLN’s subsidy burden could be reduced through more cost reflective electricity tariffs, but changes to retail prices could be tempered through better utilisation of existing generation, more focus on slowing demand growth and less dramatic expansion of capacity with contractually onerous terms.

Priority 2: Improving the bankability of projects, especially for renewables

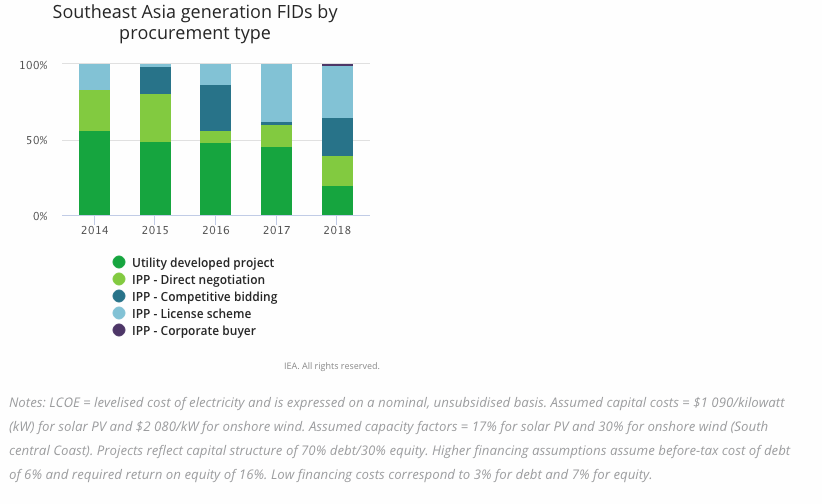

Investment frameworks for power generation have evolved considerably, but further reform could help improve bankability. While independent power producer (IPP) investments are playing an increased role, these have come mostly through administrative mechanisms, such as direct negotiation with utilities, which are often not transparent in terms of price formulation. Price incentives (e.g. feed-in tariffs) under licensing schemes have driven most investment in renewables, but their design is not always effective; in some cases (e.g. Indonesia) tariffs have been set too low to attract investment at current project costs. Competitive auctions, which can provide transparent price discovery and clear risk allocation through contracts, have helped drive down renewable purchase prices around the world, but most Southeast Asian countries have been slow to adopt this mechanism.

The case of Viet Nam illustrates challenges and opportunities in terms of policy design and bankability. Despite attractive feed-in tariffs – which spurred a boom in solar PV deployment (mostly by local developers) in the first half of 2019 – financing costs are relatively high and international banks remain reluctant to lend to renewables projects. This stems from risks associated with the power purchase agreements, including areas related to dispatch and payments, as well as concerns the adequacy of local grids to accommodate a rapid increase in variable generation. Better policy design, system integration and contractual measures could help to improve the affordability of investments. With financing terms equivalent to those found in more mature markets, generation costs for solar PV and onshore wind could be around one-third lower.

Priority 3: A supportive financial system to reduce the cost of capital for clean energy

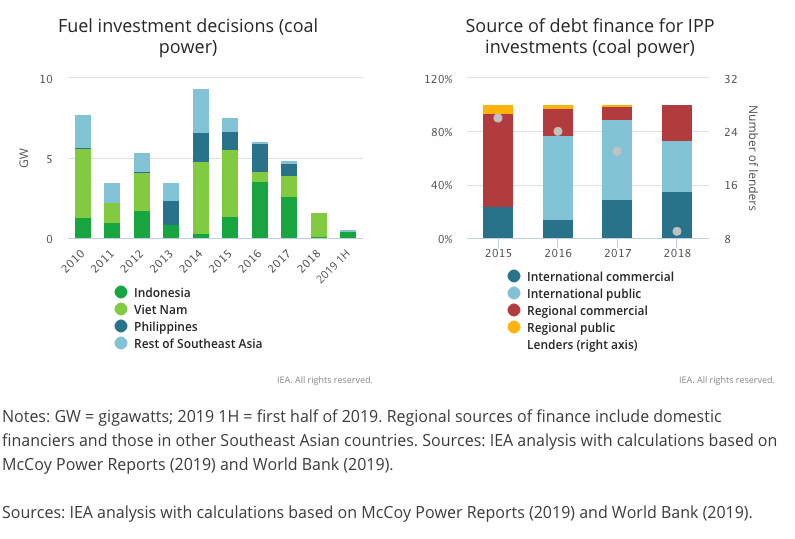

As changing financing conditions make investment in some legacy parts of the power system more difficult, more effort is needed to cultivate a supportive financing environment for newer technologies that would support capital reallocation—while ensuring security of supply Final investment decisions for coal power in the region fell to their lowest level in over a decade in 2019 (reflecting a mixture of increased financial scrutiny by banks and overcapacity concerns). There has been a reduction in the number of financiers involved in transactions in the past three years, while IPP projects that have gone ahead continue to rely on a high share of international public finance.

At the same time, mobilising capital in newer areas requires improving the cost and availability of finance. The average loan duration in Southeast Asia is just over six years, far less than the lifetimes of energy and infrastructure assets. The cost of capital for an indicative IPP varies widely – with estimates in Singapore, Thailand and Malaysia at 3-5% (nominal, after-tax), while those for Philippines, Viet Nam and Indonesia are much higher (7-10%). Investors cite limited availability of early stage project development equity and long-term construction debt for renewables and storage, though some dedicated funds, such as the Southeast Asia Clean Energy Facility, are emerging to fill the gap.

Priority 4: Integrated approaches to investment that address the demand side

Integrated approaches to investment, which take into account the demand side, could help to address rising consumption needs more cost-effectively. This is particularly true in fast growing areas, such as demand for cooling, which is a major driver of supply requirements during peak periods. But there are barriers to financing efficiency due to the small transaction sizes and challenges in evaluating the creditworthiness of consumers. Low and subsidised retail power tariffs can also distort the investment case.

Addressing information barriers, enhancing financing models and reducing subsidies would better support investment. For example, energy service companies are addressing the scale challenge of investment and have become well established in markets with long-term savings targets and supporting regulations, such as in Malaysia, Thailand and Singapore. Targeted use of public funds, insurance and capacity building can help reduce performance-related risks, as in Indonesia’s Energy Efficiency Project Finance Program. Progress in aggregating and securitising projects, through green bonds for example, could also help attract lower cost finance from a bigger pool of investors. Despite picking up in 2018, with over 40% targeting low-carbon buildings, Southeast Asia accounts for only 1% of global green bonds issuance to date.

Higher investments can be compensated with multiple benefits

Overall, achieving Southeast Asia’s energy goals will call upon stronger policy ambitions across a range of energy sources and significant new capital commitments in the years ahead. These efforts would also yield multiple benefits – in the Sustainable Development Scenario, average annual capital spending of around $150 billion over 2019-40 (higher than the $120 billion under the State Policies Scenario), is offset by the nearly $200 billion that Southeast Asian economies save annually on fossil fuel imports by 2040. Such financial savings would come in addition to improved local air quality and universal energy access, as well as a reduced contribution to global climate change.

There is now an opportunity for investors and companies in Southeast Asian countries to engage with governments in order to encourage financial decisions and policy making that are better aligned with sustainability goals. This includes not just traditional utilities, developers and banks, but also the crucial perspectives of development finance institutions and the institutional investors, whose participation will be critical to funding the region’s energy goals.

As the world’s “All-fuels and All-technologies” energy authority, the IEA will continue to assist ASEAN Member States to tackle their energy policy challenges, including through good data and analysis, training and capacity building and engagement with such communities.

Be the first to comment