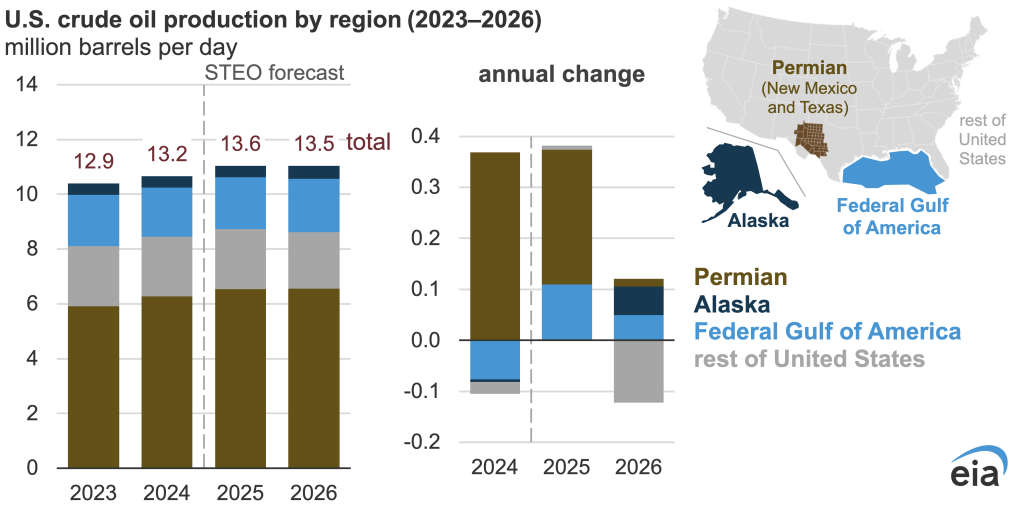

U.S. crude oil production is expected to decline slightly in 2026 following four consecutive years of increases, according to the U.S. Energy Information Administration’s (EIA) latest Short-Term Energy Outlook (STEO). The agency’s December 2025 forecast projects average production of 13.5 million barrels per day (b/d) in 2026 — roughly 100,000 b/d lower than in 2025.

The EIA attributes the shift to uneven regional performance across U.S. basins. Although modest gains are expected in Alaska, the Federal Gulf of Mexico and parts of the Permian Basin, those increases will be offset by declines in other major producing regions. Production in 2024 grew by 300,000 b/d, followed by a 400,000 b/d increase in 2025, driven primarily by the Permian Basin in Texas and New Mexico, which remains the country’s most prolific oil-producing region.

Production outlook reflects price environment

The EIA expects a softer price environment to influence drilling and investment decisions through 2026. The agency forecasts West Texas Intermediate (WTI) crude prices to average US$65 per barrel in 2025 and US$51 in 2026, down sharply from the 2024 average of US$77/b. Lower prices typically weigh on capital spending, especially among shale producers with higher costs or more marginal wells.

Reuters reporting throughout 2025 has noted that U.S. shale companies have become more sensitive to price swings as they prioritise investor returns over rapid production growth. Many publicly traded operators have tightened spending plans and focused on free-cash-flow stability, a break from the high-growth strategies seen in earlier shale booms. According to Reuters, several producers have suggested they may reduce drilling activity in 2026 if prices fall toward the levels projected by EIA.

Bloomberg analysis adds that consolidation across the U.S. shale sector — including a wave of mergers and acquisitions in 2024–25 — has resulted in fewer operators controlling larger acreage positions. Analysts say this consolidation may contribute to flatter production profiles, as large companies typically pursue steadier, slower-growth development strategies.

Regional dynamics: Permian still growing, other basins softening

The EIA forecast shows the Permian Basin continuing to expand, though at a slower pace than in recent years. Technological improvements, high-quality drilling inventory and lower breakeven costs relative to other basins will sustain output in the region through 2026.

Alaska is also projected to record modest increases as new projects ramp up following multiyear development cycles. Offshore production in the Federal Gulf of Mexico is expected to rise slightly as recently completed platforms reach full output.

However, declines are forecast in other parts of the Lower 48. Several shale basins, including the Bakken and Eagle Ford, have shown signs of maturing, with reduced drilling activity, declining well productivity in some areas and more limited access to top-tier drilling locations. As a result, gains in the Permian and offshore regions are not expected to be sufficient to offset declines elsewhere.

Demand, inventories and global market context

The production forecast comes amid mixed signals for global oil demand. Bloomberg reports that world oil demand growth slowed in 2025 as efficiency improvements, electric-vehicle uptake and sluggish industrial activity weakened consumption in several advanced economies. Nonetheless, demand in emerging markets — particularly in India and parts of Southeast Asia — remained resilient, preventing a more significant global downturn.

Reuters notes that U.S. crude inventories increased modestly through 2025, contributing to downward pressure on prices. Combined with higher-than-expected non-OPEC supply growth, these inventories have helped keep Brent and WTI benchmarks in a lower trading range.

In the U.S., NPR reporting highlights how some households and businesses continue to experience cost pressures linked to energy, despite falling crude prices. Elevated refining margins and regional constraints have kept gasoline prices higher than expected in several markets. NPR also reported that diesel prices remained volatile in late 2025 due to global refinery outages and geopolitical disruptions, contributing to higher transportation costs.

Although crude prices are forecast to decline, the EIA cautions that geopolitical risks, supply disruptions or unexpectedly strong economic growth could shift prices upward, altering production incentives in 2026.

Implications for North American supply

A slight decline in U.S. production would not fundamentally alter North America’s supply position, but it signals a potential plateau after a decade of steady growth. U.S. output surpassed pre-pandemic levels in 2023 and set new records in 2024 and 2025. Even with a modest decline in 2026, production would remain historically high.

Analysts say the U.S. may be entering a phase where production levels fluctuate within a narrower band, shaped more by price cycles, consolidation and resource maturity than by explosive growth.

Outlook

The EIA’s December STEO will be revised as market conditions evolve, but the agency’s base case suggests 2026 will mark the first year of slightly lower U.S. crude output after four years of expansion. With producers adjusting to lower prices and varied regional trends, U.S. supply growth is expected to remain constrained, even as the Permian continues to anchor national production.

Be the first to comment