Pipelines that export natural gas from the Western Canadian Sedimentary Basin (WCSB) maintained high utilisation rates through 2024 and into the first half of 2025, a trend driven by elevated production and unusually cold winter conditions in export markets, according to the Canada Energy Regulator. Export systems including the NGTL System (North Gas Transmission Line), the Alliance Pipeline and the Westcoast Pipeline form the backbone of western Canada’s gas export infrastructure.

Monthly throughput and available capacity on the NGTL system

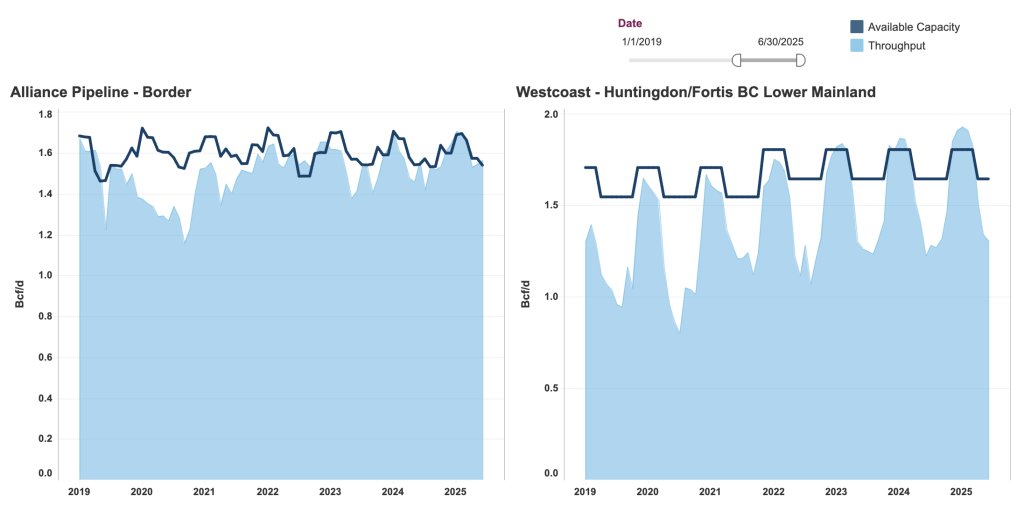

Much of the WCSB’s output must transit through key delivery points such as East Gate 1 and West Gate 2 on the NGTL system, upstream of James River, and border-points on Alliance (Elmore) and Westcoast (Huntingdon). The report notes that available capacity and throughput on the NGTL system have steadily increased in recent years, and also display a clear seasonal uptick in winter—when colder ambient temperatures compress gas molecules and demand for heating rises.

Monthly throughput and available capacity on Alliance and Westcoast Pipelines

This high-utilisation environment reflects a supply-side picture in western Canada that remains robust: producers are pumping, export pipelines are loaded, and market demand in the U.S. and beyond remains a primary driver.

The supply-demand dynamic: strong flows, underlying constraints

On the supply side, western Canada’s sustained production is feeding export corridors at full speed. The ability to ship large volumes reflects not only strong upstream activity but also favourable weather conditions in the U.S. that pushed heating demand. Cold spells in export markets added pressure to the pipeline system, enabling higher throughput.

Yet on the demand side and downstream of the pipeline system, the story is more nuanced. While export flows remain high, constraints are emerging. The CER report cautions that throughput occasionally exceeds reported “available capacity” because capacity estimates may not fully capture real-time operational conditions such as ambient temperature shifts, downstream bottlenecks or unplanned outages. This suggests that while flows are strong, the margin for additional throughput may be thin, and the system remains sensitive to weather, supply disruption or downstream demand shifts.

Be the first to comment