Alberta oil sands costs are $30-40/b, compared to $50 break even for most US shale producers

The prevailing wisdom in Alberta is that Western Canada is one of the highest cost oil and gas basins in the world. Certainly far more costly than American shale basins like the Permian in West Texas, which is attracting capital from Wall St. at a terrific rate. But Q2 reports from producers on both sides of the border reveal that oil sands producers, in particular, are far more competitive than is commonly assumed.

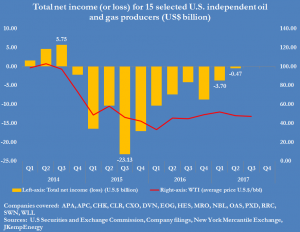

John Kemp of Reuters reports in today’s column that break even costs for Permian shale producers are hovering around $50/b, about the level where prices have settled – and appear to be settling for the foreseeable future – over the past few quarters.

“Fifteen of the largest shale oil and gas producers reported total net losses of $470 million for the three months between April and June when benchmark WTI prices averaged $48,” writes Kemp.

“Some firms claim they can break even and even make large profits with benchmark WTI prices below $50 or even $40 per barrel. It remains unclear if these figures apply to full lifecycle costs (including overheads) and all the parts of all the shale plays (or just the most productive sweet spots). However, Harold Hamm, chief executive of Continental Resources CLR.N, a large shale producer in North Dakota and Oklahoma, has said prices need to be above $50 to be sustainable.”

Ed Hirs is an energy economist with the University of Houston. He says the fact that there is so much debate about whether shale players can break even at $50 indicates that they are still on the edge at current prices.

“Break even economics do not offer anything in the way of returns to shareholders and so capital will continue to be rationed to the shale players,” Hirs said in an email in response to my questions.

“Of course, some operators will do well, but as the data show, many others are continuing to lose money. This is not sustainable.”

Permian Basin economics are better, he notes, because the geology is better than in most of the other shale basins. Plus the Permian has the advantage of multiple layers of relatively prolific stacked pays versus other shales that are limited to one or two prolific layers.

“But at sub-$50/b, it is easy to see that even the Permian is slowing down,” he concluded.

At $50, the Alberta oil sands seem primed to speed up.

For instance, Suncor Energy reported in its Q2 financials an “operating cash cost” of $27.80/b (Canadian currency). Canadian Natural Resources Limited pegged its operating cost at $22/b of synthetic crude oil. Cenovus Energy operating cost appears to be around $30/b (which I assumed was an average of $48USD WTI minus the company’s “netback,” which is defined as “gross sales less royalties, transportation and blending, operating expenses and production and mineral taxes divided by sales volumes”).

Kevin Birn, IHS MarkIt director of the Oil Sands Dialogue, points out that making an apples to apples comparison between oil sands producers and US shale producers can be difficult because of the way each employs its capital.

Shale oil wells enjoy very high production in the first 12 to 18 months, then decline rapidly thereafter. That means shale producers must always be spending a great deal of money to drill new wells to replace the lost production.

Oil sands production, however, is more like a factory. Once the companies have built the mines or SAGD fields, processing plants, and associated infrastructure (e.g. roads), then the actual cost to produce a barrel of oil is quite low. And the more the “factory” produces, the lower the cost per barrel.

“If you have an asset in the oil sands, we think most producers are somewhere between $30 and $40 on a cash cost basis. The majors (like Suncor, Cenovus, CNRL) are at the bottom-end of that range. They tend to be fairly correlated in terms of efficiency,” he said in an interview.

“On the top end, less efficient producers might be closer to $50.”

Wait, there’s more good news for oil sands producers.

While shale companies have seen their operating costs grow in the last two or three quarters because service company and input (e.g. frack sand) costs have risen from unsustainable levels, the oil sands operators are busy optimizing to bring costs down even further.

Birn says the biggest cost for a SAGD or mining operation is down time, when there is no or reduced output.

“What costs money in a manufacturing facility? When the thing doesn’t run. Because you pay for everything that’s going on in a facility but you’re not producing anything,” he said.

“So a lot of the cost reductions we’ve seen on the operating side – like the 50% reduction in SAGD operating costs since 2014, which is massive – we think has come from focusing on operational efficiency. There’s a huge potential for more of that. It’s all about standardization and predictability.”

A recent study from the Canadian Energy Research Institute estimates that over the next decade or so, SAGD producers can lower costs by 34 to 40 per cent by replacing natural gas and steam (to soften the bitumen and make it flow) with solvent (light hydrocarbons).

The Canadian oil sands producers’ attitude toward the resource is summed up by Suncor’s Fiona Jones, general manager, sustainability, in the company’s 2016 sustainability report: “So while often characterized as the oil basin most vulnerable to a low oil demand scenario, the very long operating life and low decline rate of our assets are, paradoxically, a competitive advantage – both under a scenario of declining demand for crude oil and a correspondingly low oil price, or over an extended period of uncertainty and price volatility.”

No wonder Suncor and Cenovus paid a combined $32 billion recently to purchase the oil sands assets of Shell Canada and ConocoPhillips.

The Canadian companies (and investors who financed the purchases) know a good deal when they see it.

It was actually CNRL that bought Shell not Suncor as stated.