Partially upgrading every barrel of oil sands bitumen could make Alberta much more competitive in US markets

Partially upgrading every barrel of oil sands bitumen could make Alberta much more competitive in US markets

Oil’s not going anywhere in a hurry, according to the International Energy Agency in its new World Energy Outlook. Not even widespread adoption of electric vehicles puts a dent in oil consumption before 2040. But the big news from the IEA is the rise of the United States to become the dominant global oil and gas producer. Is it time for Alberta – and Canada – to rethink the strategy of chasing overseas markets with low value oil sands bitumen?

“Electric vehicles (EVs) are in the fast lane as a result of government support and declining battery costs but it is far too early to write the obituary of oil, as growth for trucks, petrochemicals, shipping and aviation keep pushing demand higher,” said Dr Fatih Birol, IEA executive director, in a press release.

“The US becomes the undisputed leader for oil and gas production for decades, which represents a major upheaval for international market dynamics.”

“The US becomes the undisputed leader for oil and gas production for decades, which represents a major upheaval for international market dynamics.”

Americans call it the Shale Revolution for a reason. Just a decade ago US oil production was languishing at five million b/d, now it’s pushing nine million b/d. The IEA estimates that by 2040 the US will be pumping 15 million boe/d (combined shale and convention production), making it the world’s largest oil producer.

That’s right, Alberta, the blue-eyed sheikhs now live in Texas.

The US Energy Information Administration reports that since President Barack Obama – the Great Satan of the American energy industry – lifted the 40-year old oil export ban in 2015, the United States is now exporting two million b/d of crude. That number is expected to go way up in coming years, with the US becoming a net exporter before 2040.

Alberta needs to think long and hard about that trend.

In particular, it needs to ask itself this question: Is the Alberta oil industry better off fighting environmentalists and local governments over pipelines to tidewater where producers might earn an extra buck or two selling dilbit or partially upgrading bitumen into a medium or heavy crude that earns a $10 to $15 a barrel “uplift” and frees up 30 per cent of existing pipeline capacity, then backfilling American markets?

We’ve reported on the School of Public Policy study (here and here) earlier this year that showed there are as many as 10 partial upgrading technologies in the pre-commercialization stage, all of them probably five to 10 years away from being viable and scale-able.

We’ve reported on the School of Public Policy study (here and here) earlier this year that showed there are as many as 10 partial upgrading technologies in the pre-commercialization stage, all of them probably five to 10 years away from being viable and scale-able.

The study examined the economics of a 100,000 b/d partial upgrader based on MEG Energy’s HI-Q technology. A big advantage of partial upgrading is the relatively low capital cost, between $3 billion and $5 billion, and the fact it can be built in modules, so no need to construct huge “white elephants,” plants can be built as the market needs them.

Odds are the market will need them sooner rather than later: Alberta oil sands bitumen output will be around 3.4 million b/d by 2030.

Instead of the current obsession with east and west coast pipelines, imagine an alternate scenario where all of that bitumen is partially upgraded and shipped south. (while you’re at it, imagine the impact on the Alberta economy of building 38 100,000 b/d partial upgraders at a cost of $5 billion each. That’s $190 billion by my calculations.)

If it fetches up to $15/b more and enjoys reasonable pipeline tolls in the $7/b range, might the economics be better than higher tolls to tidewater, then two to four dollars to ship by tanker to Asian markets?

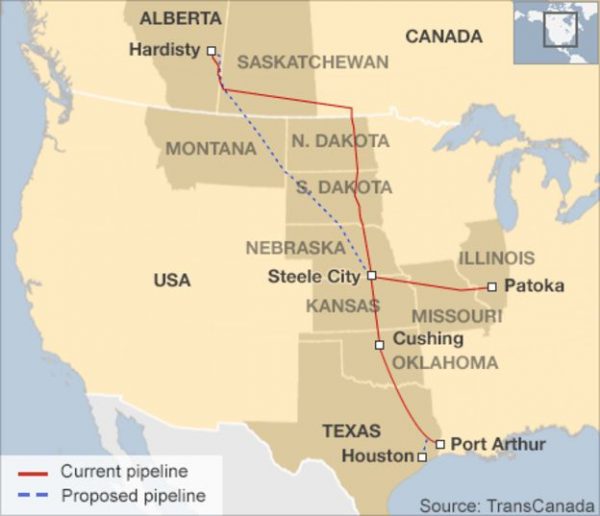

Assuming Keystone XL is built from Alberta to the Texas Gulf Coast, could it be twinned after 2030?

Is it reasonable to assume that if oil sands producers are successful in lowering the carbon-intensity of their product by 30 to 33 per cent – as they’ve committed to do and the Alberta government is preparing to incent with a carbon levy and output-based allocations – then Alberta can fend off the “dirty oil” accusation that helped sink KXL in 2015?

The answers to all these questions might be negative.

But what’s the harm in asking them and entertaining the possibility that the answers might be positive, meriting a change of course by Alberta in the very near future?

Asking the questions is even more imperative because of the scenario painted by the IEA.

From now until 2040 there will be steady growth in global consumption, driven almost entirely economic development in Asia, but there will also be significant growth in supply, driven by our friends south of the border.

Maybe it’s time to ditch Stephen Harper’s boast that Canada is an energy superpower and accept the reality that we’re really just a cog (albeit a big one) in the United States energy machine.

If we accept that reality, then our goal becomes squeezing every nickle out of the market we have, rather than chasing markets we don’t have, markets in which the Americans will be likely be much more competitive.

Consider this analysis from the IEA report:

In our projections, the 8 mb/d rise in US tight oil output from 2010 to 2025 would match the highest sustained period of oil output growth by a single country in the history of oil markets. A 630 bcm increase in US shale gas production over the 15 years from 2008 would comfortably exceed the previous record for gas. Expansion on this scale is having wide-ranging impacts within North America, fuelling major investments in petrochemicals and other energy-intensive industries. It is also re-ordering international trade flows and challenging incumbent suppliers and business models.

Is it time to reconsider Alberta’s oil production and export business model?

The industry asks and has answered the question many times, the answer upgrading when it had to, small heavy demand, when it has open markets it does not.

In addition to better economics to sell heavy the carbon foot print of upgrading is amongst the largest of full cycle crude carbon. Can you imagine increasing Canada’s carbon footprint to subsidize the downstream country?

The issue is as noted more pipe, broader markets. The value creation vs cost beats upgrading economics.

Emerging technology to improvr transportation is a bright window than the world of subsidized upgrading where tax dollars go to die

World scale refining with a breadth of crude supply & consumers is on the Gulf & Asia tidewater. In addition to environmental squeeze out, this is why Europe imports.

Glen

Have you read the School of Public Policy paper? It argues the opposite: 17% well to wheels reduction in GHGs, $10 to $15/b uplift in value, etc. I have no doubt your comments apply to full upgrading, but my interview with Kent Fellows, one of the co-authors, suggest they do not for partial upgrading. That said, the technology is 5-10 years from commercialization, so who knows?