Canadian juniors, intermediates will struggle and that’s negative for services spending, which in turn is very negative for oil patch employment

Last week, Canada’s biggest oil and gas producer was reporting record revenue of $10.3 billion and eye-popping net earnings of $5.4 billion for 2019. This week, CNRL is battening down the hatches, hoping like other Canadian producers that the global price war blows over as quickly as possible.

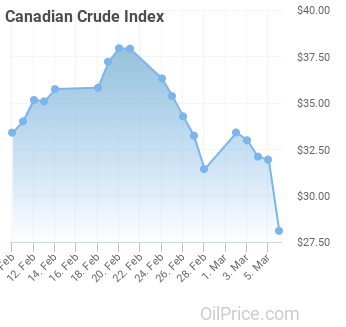

Oil prices started falling Friday after news broke of the spat between Saudi Arabia and Russia over production cuts. US benchmark West Texas Intermediate fell almost $20USD from the mid-40s before recovering to $31 by noon on Monday. Heavy oil benchmark Western Canadian Select fared just as poorly, dropping below $20USD on Monday.

“The coronavirus crisis is affecting a wide range of energy markets – including coal, gas and renewables – but its impact on oil markets is particularly severe because it is stopping people and goods from moving around, dealing a heavy blow to demand for transport fuels,” Dr Fatih Birol, the International Energy Agency’s executive director, said in a press release forecasting global oil demand to contract by 90,000 barrels per day in 2020.

“This is especially true in China, the largest energy consumer in the world, which accounted for more than 80% of global oil demand growth last year. While the repercussions of the virus are spreading to other parts of the world, what happens in China will have major implications for global energy and oil markets.”

Energi Media turned to economists Kevin Birn of IHS MarkIt in Calgary and Ed Hirs of the University of Houston for more insight into the impacts of the downturn on Canada and the United States.

Markham: What’s the background of the oil price war?

Birn: This started with an unprecedented decline in demand of crude oil all precipitated by the coronavirus wiping out demand in the world’s largest consuming region for oil, which is China. The scale of that oil market demand shock was remarkable. Then Saudi Arabia discovered it no longer had a dance partner in Russia. That pushed the market into a price war.

There are other key uncertainties facing oil markets right now. You still have sidelined oil from Libya and Iran that could come back on the market. We still don’t really understand the trajectory of the coronavirus and how it could influence demand during the back half of 2020 . We know that in China the number of cases is falling, but it’s growing in the rest of the world. That could have demand implications elsewhere and continue this oversupply situation.

Markham: What are the likely impacts for the Canadian oil and gas sector?

Birn: It’s an instantaneous demand shock and it’s been an instantaneous price drop. I think it’s important to remember that Western Canada is accustomed to incredible price volatility, the likes of which the world doesn’t get to enjoy typically. Over the past five years, we’ve seen three periods of prices in the low twenties and in pushing the teens: 2016, the end of 2018, and now in early 2020.

What it means is a contraction or a rapid reduction in the availability of cash flow and capital. We don’t have nearly as many projects as we once had and those we do have are going to be delayed or deferred. That includes the conventional and unconventional won’t have the cash flow to drill wells. Drilling activity could even go lower.

In the oil sands, capital plans are going to be deferred. At the prices we’re seeing today, if you’re making money, you’re not making much. It’s going to be another really tough year.

Markham: What about the junior oil and gas sector, which has been contracting for several years and is now facing a capital crisis?

Birn: Over the past five years, investors have generally been disenchanted with upstream oil and gas because, generally speaking, it has not been able to generate satisfactory returns, if any. US tight oil has drilled away any profitability. That’s been complicated in Canada because we’ve had the additional challenge of egress [pipelines], which reduces the attractiveness of Canada relative to its peers.

The sector has had this reduction in the availability of capital and now you have a price that won’t be able to support capital plans to continue or maintain any production volume. If you lose volume, you lose revenue, which makes it harder to dig yourself out of that hole unless you get capital or prices coming back. It’s not a pretty situation at this point.

Markham: What about the oil sands?

Birn: Scale definitely helps in this situation. It’s quite different 2014 and 2015. For most of the companies, their cash flow was limited and they spend everything they had bringing you on additional projects. When oil prices fell, they continued putting capital into those projects even as prices declined. In this case, there’s very few if any projects going on in the oil sands. The 2019 free cash flow from a lot of the major oil sands producers was very impressive, $3 billion or $4 billion in free cash flow from some.

This time, they’re going into the downturn with a bit of cash in the bank account and having significantly driven down costs from their operations. They’re more capable of weathering the storm. But it doesn’t mean it’s going to be fun.

Markham: Will there be a big impact on jobs in the Canadian oil patch? February job numbers were released Friday and Alberta alone has lost almost 13,000 positions over the past 12 months.

Birn: You’re going to see companies pull back on anything they were doing. It’s negative for employment. The juniors and intermediate producers are going to struggle and that’s negative for spending in the service sector, which is not helpful for any kind of employment recovery.

Be the first to comment