Competitors of Alberta heavy crude oils – Venezuela, Iran, Iraq – subject to risk caused by geopolitical tensions

With global oil markets now largely rebalanced, risks to oil prices, including the geopolitical risks grabbing news headlines in recent months, have become more acute. S&P Global Platts provides a special FACTBOX round-up of the top geopolitical threats by country.

“Increased West Africa, Libya and U.S. shale production are offsetting falls in supply from Venezuela, China, Egypt, Brazil’s Campos basin and North Sea,” according to Chris Midgley, global head of analytics, S&P Global Platts.

“At the moment we do not see oil prices returning to levels seen pre-2015 despite the market looking tight with stocks below 5 year average. As seasonal demand jumps almost 3 million barrels per day during the northern hemisphere summer we expect Brent oil prices to test the $75-$80-per-barrel range, but may find further support from increased supply disruption and increasing geopolitical risk.”

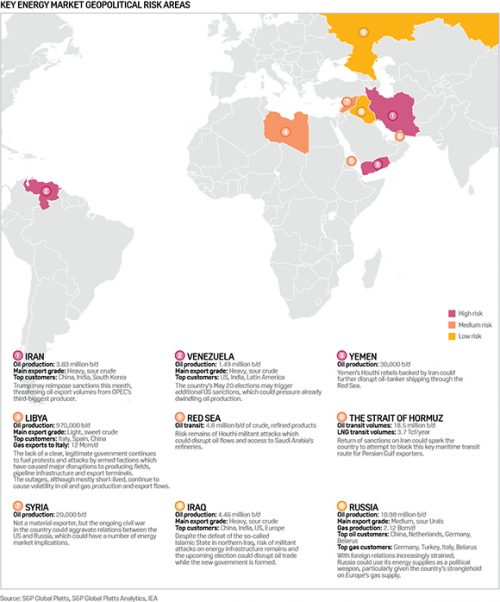

IRAN

- Production: 3.83 million barrels per day (b/d)

- Main export grade: Heavy sour crude

- Top customers: China, India, South Korea

Most Iran nuclear deal watchers expect U.S. President Donald Trump to re-impose oil sanctions on Tehran. Iran’s oil output has regained most of its previous market share since sanctions were lifted in January 2016, growing 1 million b/d to hover near 4 million b/d.

The oil market continues to react sharply to any new signals from the White House, the deal’s European partners, or Tehran ahead of May 12, the deadline for Trump to decide whether to continue waiving sanctions.

Renewed U.S. sanctions would likely have an immediate impact on crude exports from Iran, OPEC’s third-biggest producer. Upstream investment in the country has already slowed considerably on expectations of a U.S. exit from the deal.

VENEZUELA

- Production: 1.49 million b/d

- Main export grade: Heavy sour crude

- Top customers: U.S., India, Latin America

Venezuelan output has dropped by around 40% over the last two years from 2.35 million b/d, as lower prices and a crippled economy prevent investment. The U.S. has said that it may impose further sanctions if it believes democracy is being undermined there.

The country’s May 20 elections were expected to be a trigger for potential new sanctions, which could target oil or refined product flows.

Historically a major buyer of Venezuela’s oil, especially on the U.S. Gulf Coast, U.S. refiners have been diversifying their supplies, importing heavy crudes from new markets as Venezuelan supply dips.

U.S. refiners imported 438,000 b/d of Venezuelan crude in January, with five Gulf Coast refineries taking 92% of the total, Energy Information Administration data shows.

IRAQ

- Production: 4.46 million b/d

- Main export grades: Heavy sour crude

- Top customers: China, India, U.S., Europe

Simmering tensions with semi-autonomous Kurdistan in northern Iraq has hit oil exports via Turkey. Despite the defeat of the so-called Islamic State (IS), the risk of attacks from militants on energy infrastructure continues to weigh. Recent disruption has been the result of short-lived strikes and local protests.

The potential for a new push by Baghdad to take control of oil fields in Kurdish areas is also a risk.

The upcoming elections later this month are also a short-term risk, delaying contracts while the new government is formed.

RUSSIA

- Oil production: 10.98 million b/d

- Main export grade: Medium sour Urals

- Gas production: 2.12 billion cubic meters per day (Bcm/d)

- Top oil customers: China, Netherlands, Germany, Belarus

- Top gas customers: Germany, Turkey, Italy, Belarus

Russia is the world’s biggest oil producer and supplies more than a third of Europe’s gas. Its political relations with the West are widely seen as having sunk to Cold War lows in the wake of accusations of political meddling in the 2016 U.S. elections and the alleged poisoning of a former Russian spy in the United Kingdom (U.K.).

While Moscow dismisses any suggestions of political risks to its oil and gas exports, lingering concerns remain over the potential to use energy supplies as a weapon.

Russia’s gas supply cut-offs to Ukraine in 2014 and 2015 over a pricing dispute are widely cited as an example. Should relations with Europe deteriorate further, the potential for Russia to hike its gas export duties is seen as a supply risk for the region.

STRAIT OF HORMUZ

- Oil transit volumes: 18.5 million b/d

- Liquefied natural gas (LNG) transit volumes: 3.7 trillion cubic feet per year (Tcf/year)

The Strait of Hormuz is the key maritime transit route through which Persian Gulf exporters (Saudi Arabia, Iran, Iraq, Kuwait, Qatar, the United Arab Emirates (UAE), and Bahrain) ship their oil.

The U.S. Energy Information Administration (EIA) estimates that 18.5 million b/d, or about 30% of all seaborne oil exports, passed through the choke point in 2016 mainly to customers in East Asia. Almost a third of global LNG supplies also pass through the waterway. Qatar dominates LNG export flows through the Gulf with the UAE shipping smaller volumes.

Bordered by Iran and Oman — at 21 miles wide — only Iran and Saudi Arabia have alternative access routes to maritime shipping lanes.

In the past, Iran has threatened to block shipping access to the Gulf by closing the waterway as tension over Western oil sanctions simmered. Although strategists believe Iran would struggle to blockade the choke point given the constant U.S. naval presence, a return to U.S. oil sanctions could spark fresh retaliatory threats from Tehran.

RED SEA

- Oil transit: 4.8 million b/d of crude/products

The war in Yemen has raised concerns over the Red Sea. Some 4.8 million b/d of oil and products passed through the area in 2016, representing nearly 5% of global maritime trade, according to the EIA.

Around 1.5 million b/d of crude oil mainly from Saudi Arabia, Kuwait, UAE and Oman moves south from Ain Sukhna on the Red Sea to Sidi Kerir on the Mediterranean in northern Egypt via the SUMED pipeline. The bulk of Europe’s crude oil imports from the Middle East arrive through this pipeline.

As well as being a key transit route for oil, the Bab-el-Mandeb Strait is also critical to Saudi Arabia’s own Red Sea refineries, which are largely supplied with crude oil produced in its eastern region shipped from the Persian Gulf.

Be the first to comment