This article was published by the Canada Energy Regulator on March 25, 2020.

As of Friday 20 March 2020, the spot price for West Texas Intermediate (WTI) crude oil decreased by 65 per cent from its price on 6 January 2020. Over the same time period, the price for Western Canadian Select (WCS) crude oil in Alberta fell by 72 per cent from US$40 per barrel (US$/bbl) to US$11/bbl.

In particular, on Monday 9 March 2020, the WTI price fell to US$31/bbl(1); down 25 per cent from the previous Friday. Oil prices have been falling for other benchmark crudes around the world as well. Two major market events are responsible.

Firstly, attempts to contain the COVID-19 virus, including travel restrictions, significantly decreased world crude oil demand since early January. The World Health Organization declared COVID-19 to be a pandemic and markets are expecting oil demand to decrease further.(2)

Secondly, on Friday 6 March 2020 OPEC+ nations did not agree to continue limiting oil production past March 2020. As a result, OPEC countries, including Saudi Arabia and the United Arab Emirates will increase production.

The UAE will increase production by 1 million barrels per day (MMb/d) and raise total production capacity to 5 MMb/d. Saudi Arabia will increase production capacity by 1 MMb/d to a total of 13 MMb/d.

This essentially ends the previous 2.1 MMb/d of OPEC+ production cuts in place since September 2016,(3) and may result in excess world oil supply in the near term. OPEC+ includes major crude oil exporting countries officially included in OPEC, as well as additional large producers who have coordinated with OPEC in the past such as Russia.

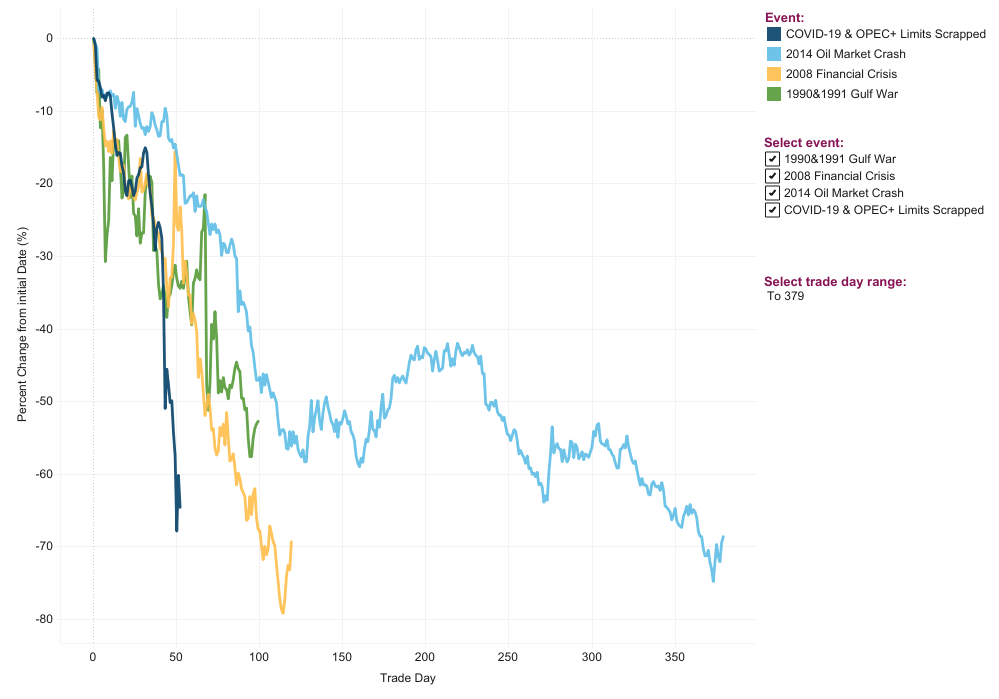

Description: The line chart follows the percentage decline in WTI crude oil prices over the course of several market events. During the Gulf War of 1990 and 1991 the price declined from US$41.07/bbl on 11 October 1990 to US$17.43/bbl on 25 January 1991, a total decline of 58% over 95 trading days until prices began to recover. During the financial crisis in 2008, the price declined from US$145.2/bbl on 14 July 2008 to US$30.3/bbl on 23 December 2008, a total decline of 79% over 114 trading days until prices began to recover. During the oil price beginning in 2014, the price declined from US$105.7/bbl on 28 July 2014 to US$26.7/bbl on 20 January 2016, a total decline of 75% over 373 trading days until prices began to fully recover. During the COVID-19 virus outbreak, the price declined from US$63.3/bbl on 6 January 2020 to US$22/bbl on 20 March 2020, a total decline of 65% over 52 trading days.

So far, this price drop has been sharper in magnitude compared to other declines, but it is not unprecedented. Below are some other historic events with similar price impacts:

- 1990-91 Gulf War: Iraq invaded Kuwait on 2 August 1990, removing 4.3 MMb/d of oil production from the market (approximately 6.5 per cent of global demand at the time(4)) when the United Nations imposed sanctions. This resulted in WTI crude oil increasing by 166 per cent from US$15/bbl in June 1990 to US$41/bbl in October 1990, a period of less than four months. Prices then fell by 58 per cent over the subsequent five months to US$18/bbl in February 1991, after a coalition of forces including Canada, and led by the United States (U.S.), became involved in the Gulf region in mid-October 1990. Oil prices started falling and largely kept falling through the subsequent invasion and war, including a one day decline of 33 per cent on 17 January 1991, as Operation Desert Storm began.

- Global financial crisis and the Great Recession: From mid-July 2008 until December 2008, WTI fell by 79 per cent from US$145/bbl to US$30/bbl, a period of less than six months. Prior to and during the early stages of the financial crisis, crude oil prices rose rapidly from high world demand and a strong world economy. As the recession spread from the U.S. financial sector to other areas of the world economy, demand for energy—including crude oil—decreased. In the U.S., crude oil consumption fell by 9 per cent from 2007 to 2009, while global crude oil consumption decreased by 1.4 MMb/d, or 1.6 per cent. Crude oil prices began to strengthen again in early 2009, and increased on average each year until 2014.

- 2014 Oil Market Crash: WTI crude oil reached US$106/bbl in June 2014 before falling to US$27/bbl in February 2016, a decrease of about 75 per cent over a period of one year and six months. Oil markets had become significantly oversupplied because of growing U.S. shale oil production, along with an OPEC decision in December 2015 to scrap output limits. From 2008 to 2014, U.S. oil production increased from 5 MMb/d to 8.8 MMb/d. Over this same time period, Canadian crude oil production increased from 2.7 MMb/d to 3.8 MMb/d,(5) also contributing to oversupplied markets. Global crude demand continued to increase each year during this period, but was outpaced by global supply growth.

Be the first to comment