This article was published by the International Energy Agency on Feb. 7, 2025.

By Rafael Martinez-Gordon, Energy Analyst Buildings

Chiara Delmastro, Energy Analyst Buildings

Jianlan Dou, Consultant

Global demand for heat pumps weakened in early 2024, but some regions may have reached a turning point

Globally, 2024 began as a tough year for heat pumps1, but early data from late 2024 hints at a potential recovery in some markets.

In the United States, the second-largest heat pump market, sales fell by 1 per cent in the first half of the year (H1) amid low consumer spending and a preference for repairing rather than replacing equipment. However, the market share of heat pumps continued to increase, as sales of fossil fuel systems declined further, with sales in H1 being 25 per cent lower than those of heat pumps.

In the European Union, the third-largest heat pump market, sales fell by almost 50 per cent in H1 2024, marking a second consecutive semester of declining sales. Several factors contributed to this trend, including the decline in natural gas prices, a slowdown in the construction sector—with a large share of heat pumps installed in new buildings—and an uncertain political and regulatory landscape.

In Japan, the fourth-largest heat pump market, sales increased marginally by 1 per cent in H1 2024 compared to 2023, but are showing signs of stagnation, in part due to consumer reticence. For example, the Japanese ‘willingness to buy durable goods’ index has declined over the past decade and is now well below pre-pandemic levels.

China witnessed significant growth in installations in the first months of 2024, with sales increasing by 13 per cent in H1 2024, the second consecutive year of double-digit growth, consolidating its position as the largest domestic market (30 per cent of global total). Sales in China are gaining ground in China’s national-level policies as part of the overarching plans towards carbon neutrality before 2060, and increased in all heat pump segments: air-to-air heat pumps, which are typically used for both heating and cooling; air-to-water heat pumps, which are more common in northern China; and heat pump water heaters, which are increasingly used in both residential and commercial applications.

Although global data for the full year 2024 is not yet available, some early regional data signals a slight rebound in the second half of 2024. The United States experienced a strong recovery after the summer, with sales up almost 15 per cent year-on-year by November. This rebound suggests a potential recovery after the slowdown in 2023 and the first half of 2024, but sales are still below the record levels of 2022. Early data for the full year 2024 for Germany, Europe’s second largest heat pump market, confirms the strong decline observed in H1, with sales falling by almost 50 per cent. However, the German Heat Pump Association (BWP) expects heat pump sales to increase by more than 30 per cent by 2025 as incentives and subsidies start to take effect. In Japan, early market data shows that sales increased by around 5 per cent by December 2024, recovering from a weak first half of the year. However, sales are still below 2022 levels.

This rebound, if confirmed, would consolidate a turnaround in global heat pump markets, which, after peaking in 2022, declined in 2023.

Heat pump supply chains are less concentrated than most other clean energy technologies

Heat pumps are largely produced in the regions where they are installed, with manufacturing capacity less concentrated geographically compared with other clean energy technologies such as solar PV and batteries.

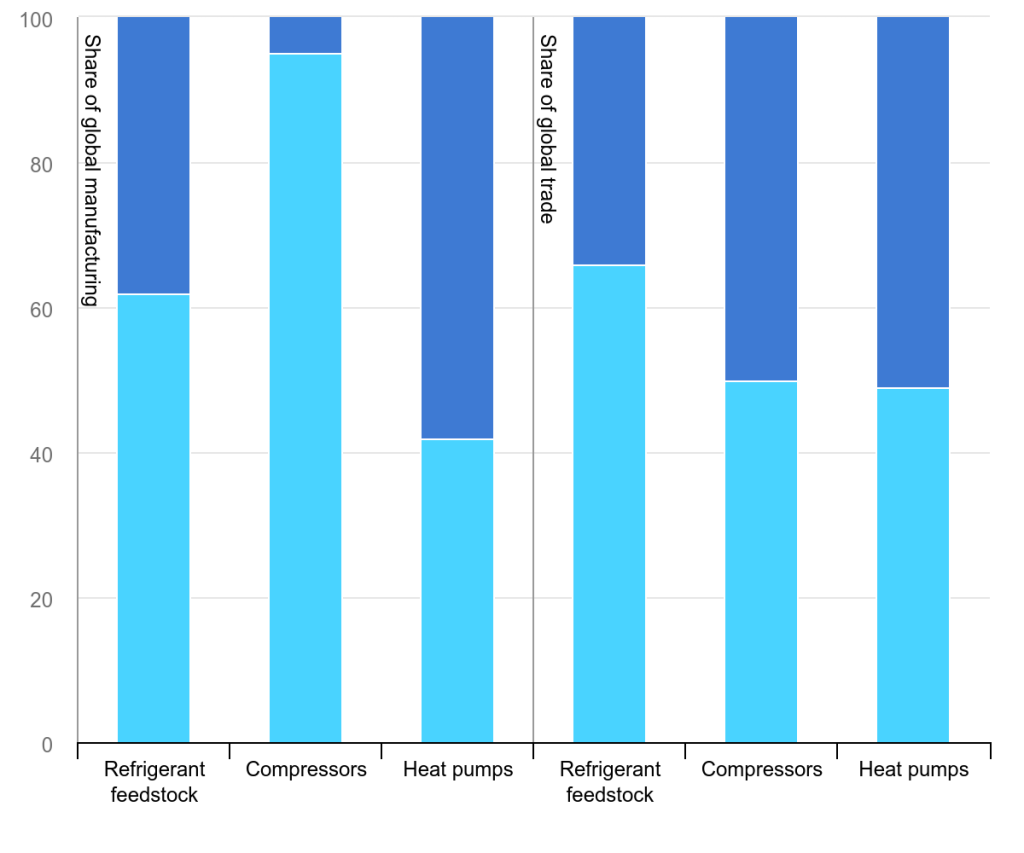

Despite this, in 2023, 40 per cent of heat pumps sold globally were manufactured in China, more than the heat pumps manufactured in the European Union (15 per cent of the global total) and the United States (20 per cent) combined. In most regions heat pump manufacturing capacity additions were minor in 2023, but in China, they increased by over 10 per cent, following an uptick in domestic demand witnessed in the same year. China imports very few heat pumps from other countries, and the market’s self-sufficiency has been maintained in recent years, despite domestic demand and exports increasing by around 10 per cent since 2021. In addition, China’s share of global heat pump exports was 50 per cent in 2023.

China not only holds the largest share of manufacturing capacity for heat pumps, but also for certain heat pump components. In 2023, China accounted for 95 per cent of compressors manufactured, and 50 per cent of the compressors traded worldwide in monetary terms.

Concentration along heat pump supply chains, 2023

Notes: Trade flows for compressors and refrigerant feedstock are derived on the basis of HS codes 841430 (Compressors; of a kind used in refrigerating equipment), 252921 (Fluorspar; containing by weight 97 per cent or less of calcium fluoride), and are calculated in monetary terms. Trade flows for heat pumps are based on analysis from Energy Technology Perspectives 2024 and are calculated in capacity terms. Trade flows are computed using the following regional aggregates: European Union, North America, Japan, Other Europe, China, Other Asia Pacific, Central and South America, Rest of World. Refrigerant feedstock = fluorspar.

Synergies with air conditioning manufacturing provide competitive advantage

Compared with manufacturers focused only on producing heating equipment, air conditioner manufacturers enjoy a competitive advantage when expanding into the heat pump market, given that the assembly processes for different types of heat pumping equipment – whether for units to provide heating, cooling or both – are quite similar, and they share key components like compressors or heat exchangers. They can quickly scale up production by converting air conditioner assembly lines to heat pump assembly lines and vice versa, benefiting from economies of scale, cheaper sourcing of components, an existing workforce. This opportunity is particularly notable in China, given that the country holds the largest air conditioning manufacturing capacity — over 80 per cent of the global total — and that most plants are not operating at maximum capacity, with as much as 40 per cent unutilized.

Furthermore, for the major manufacturers of air conditioners and heat pumps, the volume of air conditioners they produce is generally an order of magnitude larger than that of heat pumps targeted to the heating market. As a result, shifting a relatively small part of their air conditioning capacity could lead to a large increase in the heat pump segment.

But other factors also drive cost-competitiveness

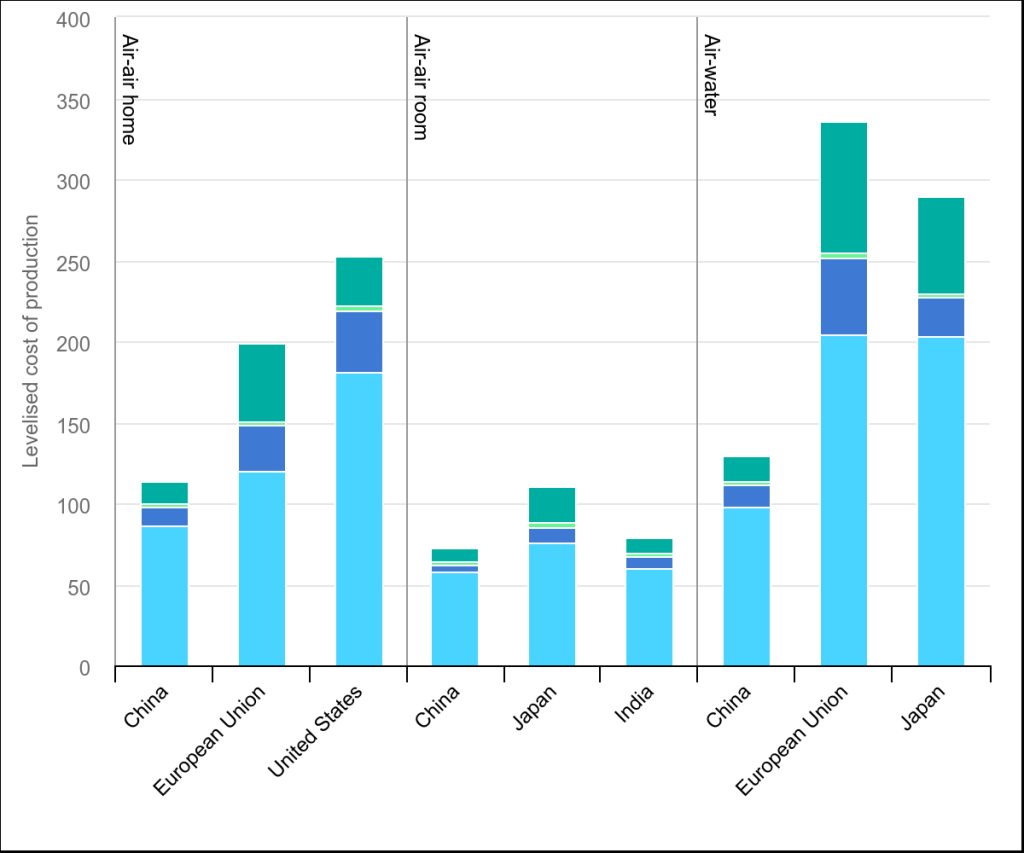

Beyond the synergies with the air conditioning markets, a number of additional factors can support investment in heat pump manufacturing, such as access to lower-cost components and to skilled labour, a stable and supportive policy environment, or the existence of adequate infrastructure. Overall, competitiveness of manufacturing can well be illustrated by comparing the levelized cost of production (LCOP) of heat pumps in different regions: On a per kilowatt basis, it is 50 per cent cheaper to manufacture an air source heat pump in China than in the United States, and 40-60 per cent cheaper than in the European Union. As heat pump assembly lines are relatively simple and don’t require advanced equipment, the capital cost of building factories (representing 1-3 per cent of the LCOP), the operating cost of keeping the lines running (10-25 per cent) and the labour cost (10-15 per cent) are not major contributors to production costs. The main cost driver for heat pumps assembly is the sourcing of components (60-80 per cent), therefore companies that can source components in-house, or take advantage of economies of scale, can benefit from lower production costs.

Levelized cost of production for heat pumps in selected countries/regions by type, 2023

Heat pump trade is set to expand, but local production will remain key in major markets

Heat pumps traded globally account for only one-quarter of all heat pump installations today, largely because local manufacturers are most familiar with local preferences, standards or even traditional building designs. China is the largest exporter of heat pumps, with exports of over 10 GW in 2023 – half of the global total traded volume. Three-quarters of these exports are to European countries, which relied on Chinese imports to meet part of the considerable increase in demand between 2020 and 2023. Exports account for one-quarter of China’s heat pump production, while the remaining three-quarters are sold domestically, covering all of China’s heat pump demand.

Trade in heat pumps has grown less rapidly than in other clean energy technologies, but as heat pump installations are set to grow in the coming decades2, international trade is likely to expand too. In the Stated Policies Scenario (STEPS), which reflects current policy settings, demand for heat pumps and international trade more than doubles in 2035. Trade activity remains limited in the United States and Japan, while Europe’s imports, notably from China, increase to around 25 GW by 2035.

However, although heat pump trade is set to increase in the STEPS, major markets are expected to continue sourcing most of their heat pumps domestically. Today, only about 25 per cent of global heat pump production is traded. This trend is expected to continue: in the STEPS, domestic production covers around three-quarters of demand in the European Union and Japan and nearly 90 per cent in the United States by 2035.

Better data can play a role in supporting heat pump deployment and shaping industrial strategies

More granular reporting of heat pump deployment and manufacturing, covering technology, capacity and building type, will be crucial for assessing market development in different regions and generating reliable information to support policy making, thereby allowing industry, policy makers and civil society to monitor whether heat pump targets are being met – and ultimately to support increased deployment around the world. Stronger international collaboration could facilitate the exchange of data and the harmonization of reporting, as well as the sharing of best practices. Better data is particularly needed for air-to-air units, which are often used exclusively for space cooling or in parallel with other heating equipment.

The lack of common definitions or a “taxonomy” for heat pumps makes it difficult to consolidate data at a global level and complicates the comparison of statistics between different markets. For example, China is the largest market for reversible air conditioners and a significant proportion of these units are used as primary heating systems. However, these units are not included in the official data statistics as “heat pumps”, whereas they are included in the official statistics of other major markets such as the European Union or the United States.

International representatives from heat pump manufacturers, industry associations, public sector and academia gathered at the IEA headquarters on 23 January 2025, to discuss how improving data quality can drive policy support, and examining how organizations can work together on data harmonization and alignment.

The IEA will continue to engage with international stakeholders to support harmonization of heat pump taxonomies and definitions and will continue to publish regular updates on global heat pump sales and deployment.

References

- Heat pumps in this commentary refer to those that deliver heat directly to households and residential or commercial buildings for space heating and/or domestic hot water provision. They include natural source heat pumps, including reversible air conditioners used as primary heating equipment. They exclude reversible air conditioners used only for cooling, or used as a complement to other heating equipment, such as a boiler.

- Despite the slowdown in heat pump sales, there are reasons to expect an upturn in the coming years, partly thanks to increasing competitiveness with alternatives and energy efficiency regulation in buildings.

Be the first to comment