By Ed Hirs

This article was published by Forbes on Oct. 20, 2020.

Oil prices have held relatively steady in recent months around $40 per barrel. This is not a bad level, as far as OPEC+ is concerned, because at that price most all U.S. oil drillers are effectively insolvent, and U.S. oil supply will continue to drop, from roughly 10.5 million barrels per day—down from more than 13 million barrels per day pre-pandemic.

Sure the OPEC nations would like to generate some more revenue, but having gone through all this pain already, they cannot afford an untimely resuscitation of the U.S. shale patch. That’s why in 2021 we can expect that OPEC+ will not proactively tighten its production to increase the oil price above $50 per barrel, the minimum necessary breakeven for many U.S shale patch operators.

In time, low prices become the solution for low prices. As both shale operators and Venezuela both become well and truly moribund and locked into terminal production declines, OPEC+ may allow the price to begin to creep upwards from current levels to $50 per barrel to encourage low-cost operators in the Middle East and around the world to return to drilling. Otherwise, declining production from existing wells will smash into a post-pandemic global recovery and drive the oil price uncomfortably high for OPEC+.

It is in the interest of OPEC+ to avoid another boom and bust cycle. Such volatility is not the friend of consumer or producer. But if the past is any guide, OPEC+ will elect to do nothing until the diminished supply creates a short term windfall for producers and a crisis for consumers.

OPEC’s December 1 meeting may bring a change in direction. The members have been hammered by the pandemic, as have all countries in the global recession. Unlike other nations, the OPEC+ members can collectively act to increase revenue.

Whether they will, and by how much, depends on several factors.

The December meeting will occur after the US election. For several years now, Saudi Arabia and Russia have acceded to President Trump’s demands for low oil prices. While this has hurt President Trump’s re-election campaign among U.S. oil companies, he knows that there are more consumers than producers. Post-election, OPEC+ – the 13-member Organization of Petroleum Exporting Countries, led by Saudi Arabia, in collaboration with a 10-member group of crude-producing countries led by Russia – may be less inclined to keep oil prices low, no matter who wins.

Market share retention and development are additional factors in the OPEC+ calculus. OPEC+ is trying to protect its current oil market share and stymie the further adoption of LNG by developing economies. While oil prices are low today, natural gas and LNG prices are relatively lower on a heat equivalent or Btu content basis—one barrel of crude oil having the Btu content of six thousand cubic feet of pipeline quality gas—or $42 per barrel of oil versus $12 for the Btu equivalent of LNG in July and $39 for the Btu equivalent of LNG, the current seasonal peak price. This does not matter in the US, where natural gas and oil are not used interchangeably. In developing economies where countries are also striving to reduce carbon, natural gas in the form of LNG can be chosen instead of oil. With a low LNG price, LNG-exporting nations can subsidize regassification facilities and hook these economies, to the detriment of oil producers. Consequently, raising oil prices would further handicap OPEC+ in growing market share.

The massive increase in the US money supply and massive fiscal stimulus approved by the US Congress in response to the Covid-19 pandemic bodes well for the dollar price of oil. As a commodity in global trade, oil trades in US dollars for all practical purposes. The purchasing power of a barrel of oil is therefore tied to the value of the US dollar. Producing countries lose purchasing power when the US dollar declines in value if they do not increase the price of oil.

The US dollar is down about 12 per cent since the beginning of the year, and inflationary pressures in the US are building. Under former Fed Chair Janet Yellen, the balance sheet of the Fed was artfully unwound following the Great Recession without either inflation or a devaluation of the US dollar. Current Fed Chair Jerome Powell will have an even more daunting task once the economy begins to turn around because Trump or Biden will consider devaluing the US dollar as a way to stimulate the economy.

Such a devaluation would increase the risk of domestic inflation if the Fed is not nimble enough. But the prospect of a declining US dollar also raises the prospect of an increasing dollar price of oil.

The Cure For Low Oil Prices Is Low Oil Prices

OPEC+ can decide to maintain current production levels and simply let nature takes it course. The current low oil prices have driven Wall Street out of the US shale patch for the foreseeable future. The contraction and consolidations will continue lessening the threat to the OPEC+ market share. Less drilling means less oil produced and lower supply, just as demand recovers when the world emerges from the global pandemic.

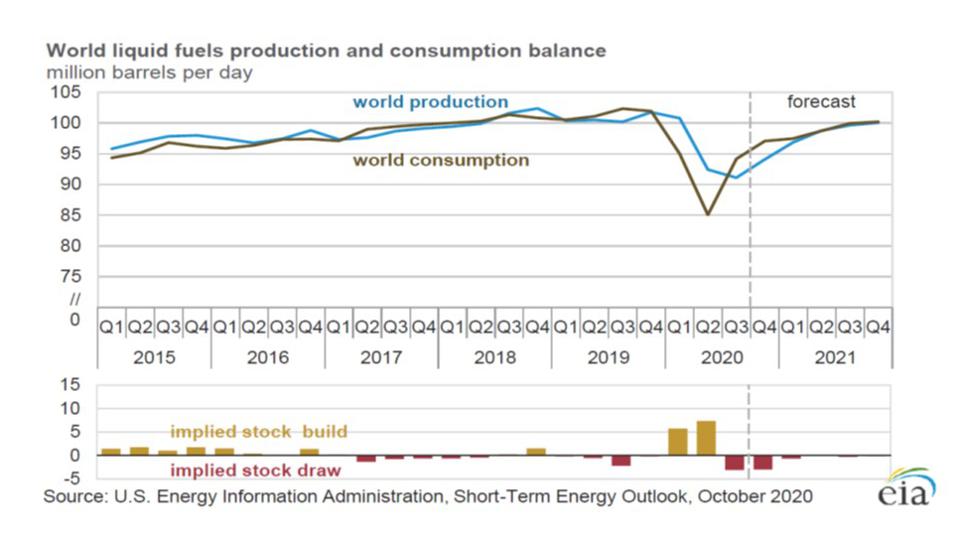

For now, rig counts are down. With a current market of approximately 94 million barrels per day, Baker Hughes BHI -1.5 per cent reports the non-US rig count is down by 40% since the beginning of the year, to 752. The stunning decline is in the Middle East, home to the most productive wells in the world, where the rig count is down from 430 to 282. The last time the world market maintained 94 million barrels per day—and was growing—was in 2014, when the Middle East averaged 406 active rigs and the total non-US rig count averaged 1,517.

Similarly In the US, the rig count is down to 257 from a September 2014 peak of 1,930. US drilling is far below the level necessary to maintain levels of production. It is just a matter of time. The members of OPEC+ know it. Patient US oil companies know it too.

Be the first to comment