Source: U.S. Energy Information Administration, Short-Term Energy Outlook, natural gas

Non-hydro renewables’ share of total US utility-scale generation to exceed 10% for first time in 2019

EIA’s Jan. 2018 Short-Term Energy Outlook (STEO) forecasts that natural gas will remain the primary source of U.S. electricity generation for at least the next two years.

The share of total electricity supplied by natural gas-fired power plants is expected to average 33 per cent in 2018 and 34 per cent in 2019, up from 32 per cent in 2017.

EIA expects the share of generation from coal, which had been the predominant electricity generation fuel for decades, to average 30 per cent in 2018 and 28 per cent in 2019, compared with 30 per cent in 2017.

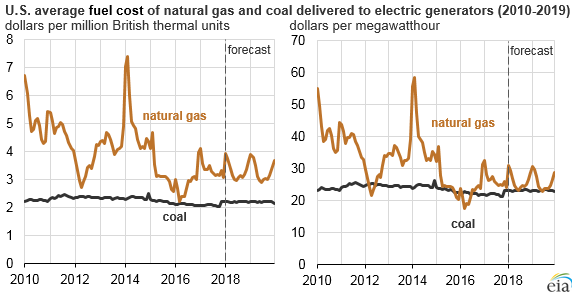

The mix of energy sources used for producing electricity generation continues to shift in response to changes in fuel costs and the development of renewable energy technologies.

Since 2015, the cost of natural gas delivered to electric generators has generally averaged $3.50 per million British thermal units (Btu) or less, and it is expected to remain near this level through 2019.

The average cost of natural gas delivered to generators in 2018 is forecast to fall 2 per cent, while the forecast delivered cost of coal rises 5 per cent.

These relative price changes should increase the share of natural gas generation in 2018. The costs of both natural gas and coal in 2019 are expected to remain relatively unchanged from this year’s forecast prices.

Power plant operators are scheduled to bring 20 gigawatts (GW) of new natural-gas fired generating capacity online in 2018, which, if realized, would be the largest increase in natural gas capacity since 2004.

Almost 6 GW of the capacity additions are being built in Pennsylvania, and more than 2 GW are being built in Texas. In contrast, about 13 GW of coal-fired capacity are scheduled to be retired in 2018.

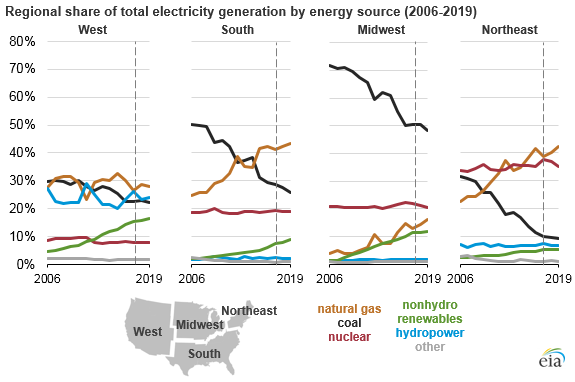

These changes in the generating capacity mix contribute to the continuing switch from coal to gas, especially in southern and midwestern states.

Compared with the rest of the country, the use of natural gas for electricity generation is not expected to increase as much in the West, where natural gas largely competes with hydropower.

EIA expects the gas generation share in the West region to rise from 27 per cent in 2017 to 29 per cent in 2018, primarily as a result of a decline of the region’s hydropower generation share, which is expected to fall from 26 per cent in 2017 to 23 per cent in 2018.

In 2017, hydropower generation in the West benefitted from atypically wet conditions.

Generation from renewable energy sources other than hydropower has grown rapidly in recent years.

EIA expects the average annual U.S. share of total utility-scale generation from nonhydro renewables to exceed 10 per cent for the first time in 2019.

Be the first to comment